TL;DR:

- Extended insurance covers mechanical repairs after factory warranties expire but varies in coverage, cost, and eligibility. It is a complex category that includes mechanical breakdown insurance and vehicle service contracts, each suited to different vehicle types and ownership scenarios. Buyers should verify provider licensing, carefully review contracts, and consider their vehicle's repair history before purchasing to ensure worth and legality.

Extended insurance is a paid protection plan that supplements or replaces your car's original factory warranty, covering costly mechanical repairs after the manufacturer's coverage expires. Most car owners first hear about it when their factory warranty is about to run out, but the decision to buy deserves far more thought than a dealership finance office allows. The industry uses two main terms: mechanical breakdown insurance (MBI) and vehicle service contracts (VSC). Both fall under the broader umbrella of extended warranty insurance, and the Federal Trade Commission (FTC) along with the Magnuson-Moss Warranty Act set the consumer protection rules that govern them. Understanding the differences before you sign anything saves you money and frustration.

What is extended insurance and how does it work?

Extended insurance is not a single product. It is a category that includes MBI policies sold by auto insurance companies and VSCs sold by dealerships, third-party administrators, and specialty providers like Rpmwarranty. Both types pay for covered mechanical repairs after your factory warranty ends, but they operate under different rules, pricing structures, and eligibility requirements.

A factory warranty from BMW, Mercedes-Benz, Ford, or Honda covers defects in materials and workmanship for a set period, typically three to five years or a defined mileage limit. Once that coverage ends, any repair bill lands entirely on you. A BMW 5 Series transmission replacement can run well above $5,000. A Mercedes-Benz air suspension failure on an S-Class can cost even more. Extended protection plans exist specifically to absorb those costs.

The Magnuson-Moss Warranty Act requires that warranty terms be disclosed clearly and in plain language. The FTC enforces rules that prevent sellers from voiding your factory warranty simply because you used an independent repair shop. Knowing these two regulatory anchors gives you real leverage when reviewing any contract.

Pro Tip: Read the definitions section of any extended protection plan contract first. That single section tells you what "covered component" means and reveals most of the exclusions before you read a single line of the coverage schedule.

What types of extended insurance options exist?

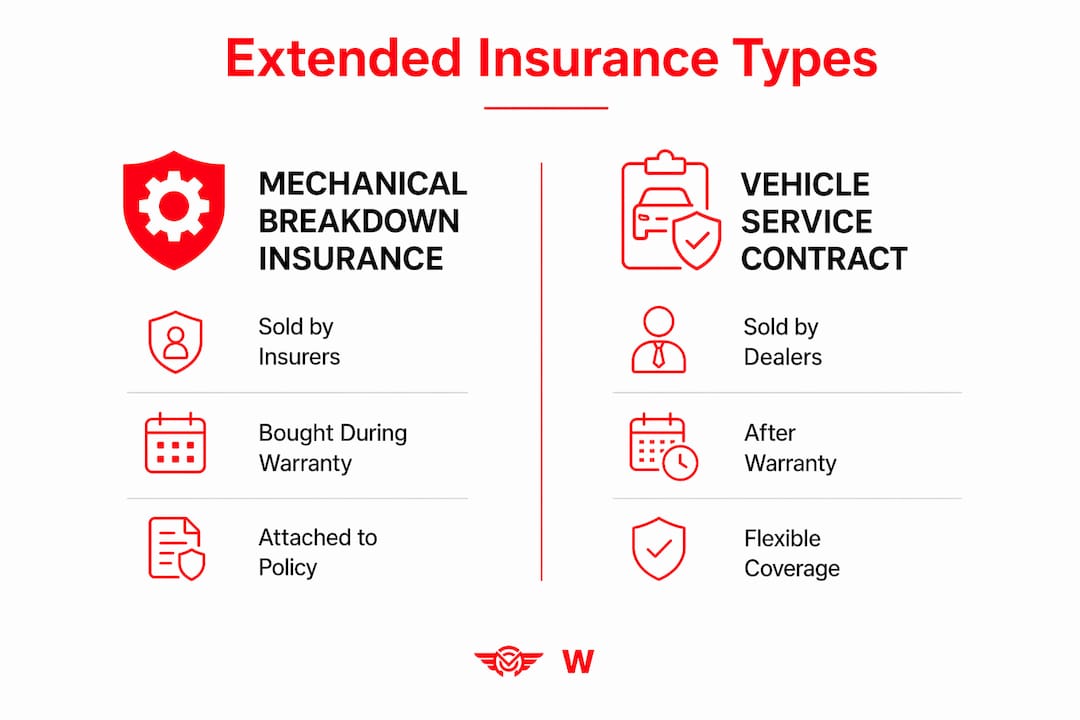

MBI and VSCs are distinct products with different purchase windows, payment structures, and repair shop rules. Knowing which type fits your situation is the first real decision you face.

Mechanical breakdown insurance (MBI)

MBI is sold by auto insurance companies and added to your existing auto policy. It typically must be purchased while your factory warranty is still active, which means the window closes fast. MBI usually allows you to choose any licensed repair facility, and you pay monthly as part of your insurance premium. MBI costs $30 to $100 per year with deductibles ranging from $200 to $500. That low annual cost reflects a significant limitation: MBI is generally not available for luxury vehicles like Porsche, Range Rover, or Mercedes-Benz, and it excludes high-mileage cars.

Vehicle service contracts (VSCs)

VSCs are the more flexible option. They can be purchased after factory warranty expiration, which means owners of older Ford F-150s, Honda Accords, or higher-mileage vehicles still qualify. VSCs come in tiers, from powertrain-only plans covering the engine, transmission, and drivetrain, to near-bumper-to-bumper plans that also protect electrical systems, cooling systems, and high-tech components. Some VSCs require repairs at network-approved shops, while others allow any ASE-certified facility.

| Feature | MBI | Vehicle Service Contract |

|---|---|---|

| Sold by | Auto insurance companies | Dealerships, third-party administrators |

| Purchase window | During factory warranty period | Before or after factory warranty expiration |

| Payment structure | Monthly, added to insurance bill | Lump sum or monthly financing |

| Repair shop choice | Usually open choice | Network shops or open choice, varies by plan |

| Luxury vehicle eligibility | Generally excluded | Available for most vehicles including luxury |

| Deductible range | $200–$500 | $50–$500 |

Pro Tip: If you drive a Honda Civic or Ford Explorer and your factory warranty is still active, MBI is worth pricing out immediately. If you drive a Porsche Cayenne or Range Rover Sport, go straight to a VSC from a reputable administrator.

How much does extended insurance typically cost?

Cost is where car owners get the most confused, and where the most money gets wasted. Powertrain-only plans cost less, while bumper-to-bumper coverage can exceed $3,000. That wide range reflects real differences in vehicle type, mileage, age, and coverage depth.

Luxury and performance vehicles cost significantly more to cover. A Porsche Panamera or BMW 7 Series carries higher repair costs and less common parts availability than a Honda CR-V. Providers price that risk into the premium. A powertrain plan for a high-mileage Ford Mustang will cost less than a comprehensive plan for a low-mileage Mercedes-Benz GLE, even if both cars are the same model year.

| Vehicle Type | Coverage Level | Typical Cost Range |

|---|---|---|

| Mainstream sedan (Ford, Honda) | Powertrain only | $800–$1,500 |

| Mainstream sedan (Ford, Honda) | Bumper to bumper | $1,500–$2,500 |

| Luxury vehicle (BMW, Mercedes) | Powertrain only | $1,500–$2,500 |

| Luxury vehicle (BMW, Mercedes) | Bumper to bumper | $2,500–$3,500+ |

| High-performance (Porsche, Range Rover) | Comprehensive | $3,000–$5,000+ |

Deductibles also shape your real cost. A per-repair deductible charges you separately for each system repaired in a single visit. A per-visit deductible charges you once regardless of how many components are fixed. If your BMW needs both an alternator and a water pump replaced at the same time, a per-visit deductible saves you real money.

Buying directly from a contract administrator rather than through a dealership removes the dealer markup, which can add hundreds of dollars to the total price. The coverage is often identical. The only difference is who collects the margin.

Pro Tip: Always ask whether the deductible applies per repair or per visit. That single question can change your out-of-pocket cost by hundreds of dollars on a complex repair job.

When does buying extended insurance actually make sense?

The honest answer is that extended warranties are priced to guarantee profitability for sellers, which means the average buyer pays more in premiums than they receive in repair benefits. That statistical reality does not make extended coverage a bad purchase. It makes it a specific kind of purchase: one that trades financial efficiency for predictability.

Extended coverage makes the most sense in four situations. First, you plan to keep the vehicle well past the factory warranty period. Second, the vehicle has a known history of expensive component failures. Third, a large unexpected repair bill would genuinely strain your finances. Fourth, you want fixed monthly costs rather than unpredictable repair expenses.

Here is a numbered checklist to assess whether extended coverage fits your situation:

- Check your ownership timeline. If you trade vehicles every two to three years, a long-term plan rarely pays off.

- Research your vehicle's repair history. BMW N63 engines, Mercedes-Benz air suspension systems, and Porsche PDK transmissions have documented repair patterns. Know what you are likely to face.

- Calculate your savings alternative. The FTC notes that some financial experts recommend saving equivalent premiums in a dedicated account instead of buying coverage.

- Assess your risk tolerance. A $4,000 transmission repair on a Range Rover Sport is a manageable inconvenience for some owners and a financial crisis for others.

- Review your current warranty status. If your factory warranty still has 12 months remaining, you have time to compare plans without pressure.

- Confirm the vehicle's mileage trajectory. High-mileage vehicles approaching 100,000 miles face higher mechanical risk, which shifts the cost-benefit calculation toward coverage.

Extended warranties function as peace-of-mind purchases rather than financial investments for most buyers. Framing the decision that way removes the confusion. You are not trying to beat the house. You are buying predictability.

What are the legal rules around extended insurance?

Extended warranties are legally classified as service contracts, not insurance, in most states. That distinction matters because service contracts fall under different consumer protection laws than insurance products. California is a notable exception: the state requires extended warranty products to be sold by licensed insurance providers, which is why California residents are typically offered MBI rather than third-party VSCs.

The Magnuson-Moss Warranty Act protects you from having your factory warranty voided simply because you bought an aftermarket part or used an independent shop. The FTC enforces this rule. Any provider that tells you otherwise is either misinformed or misleading you.

Key protections and red flags to know:

- Verify licensing. Legitimate providers are licensed by state authorities. Ask for proof before signing anything.

- Demand a sample contract. Legitimate providers always supply a sample contract before payment. Any company that refuses is a red flag.

- Reject cold calls. Real extended insurance providers do not cold-call consumers. Unsolicited calls claiming your warranty is about to expire are almost always scams.

- Check the Better Business Bureau. NerdWallet analysts recommend verifying providers through the BBB and FTC records before committing to any plan.

- Read the exclusions list. Exclusionary contracts list what is not covered. Inclusionary contracts list only what is covered. Inclusionary contracts are generally more favorable to the buyer.

- Confirm cancellation terms. Most legitimate plans offer a full refund within 30 days and a prorated refund after that. No refund policies are a serious warning sign.

The legal landscape for extended protection plans varies by state, so confirming the regulatory status of any provider in your state is a necessary step, not an optional one.

Key Takeaways

Extended insurance is best understood as a predictability tool, not a financial investment, and the right plan depends on your vehicle, your ownership timeline, and your financial risk tolerance.

| Point | Details |

|---|---|

| Know the product type | MBI suits newer mainstream vehicles; VSCs cover older and luxury vehicles like BMW and Porsche. |

| Understand real costs | Bumper-to-bumper plans can exceed $3,000; luxury vehicles like Mercedes and Range Rover cost more to cover. |

| Buy direct to save money | Purchasing from a contract administrator instead of a dealership removes markup and lowers total cost. |

| Verify legal standing | Extended warranties are service contracts, not insurance, in most states; confirm provider licensing before signing. |

| Spot scams early | Legitimate providers never cold-call; always demand a sample contract before any payment. |

My take on extended insurance after years in the industry

The biggest mistake I see car owners make is treating extended insurance as a binary decision: either buy it or skip it. The real question is which product, from which provider, at what price, for which vehicle.

I have reviewed hundreds of contracts over the years. The ones that hurt buyers most are not the outright scams. They are the legitimate-looking plans with per-repair deductibles, narrow definitions of "covered component," and exclusions buried in the definitions section. A plan that covers your BMW's engine but excludes the turbocharger because it is listed as an "excluded forced induction component" is technically legitimate and practically useless for that vehicle.

The advice I give consistently is this: if you drive a vehicle with known expensive failure points, such as a Mercedes-Benz with air suspension, a Porsche with a dual-clutch transmission, or a Range Rover with its notorious electrical complexity, extended coverage is worth serious consideration. The math changes when a single repair event costs more than the entire plan premium.

What I find genuinely undervalued is the per-visit deductible structure. Most buyers focus on the total plan price and ignore the deductible terms. On a complex vehicle like a BMW 5 Series or a Ford F-150 with advanced driver assistance systems, a per-visit deductible can save you $300 to $500 on a single repair visit compared to a per-repair structure.

Shop with patience. Read the exclusions before the coverage schedule. And never buy under pressure.

— Kenneth

Rpmwarranty offers extended vehicle protection worth considering

Car owners who want straightforward extended protection without dealership pressure have a direct option worth exploring.

Rpmwarranty provides extended vehicle warranty plans covering engines, transmissions, cooling systems, electrical systems, and high-tech components across a range of vehicles. The platform offers three plan tiers: Elite, Advanced, and Essential, each designed for different budgets and coverage needs. Flexible payment options mean you are not forced into a lump-sum commitment. Nationwide coverage and roadside assistance are included across plans. Getting a free quote takes minutes and lets you compare coverage levels side by side based on your vehicle's year, make, and model before making any commitment.

FAQ

What is the difference between MBI and a vehicle service contract?

MBI is sold by auto insurance companies and must typically be purchased during the factory warranty period, while a vehicle service contract can be purchased for older or higher-mileage vehicles after factory warranty expiration.

Are extended warranties worth buying for luxury vehicles?

Luxury vehicles like BMW, Porsche, and Mercedes-Benz carry higher repair costs and less common parts, which makes extended coverage more financially justifiable than for mainstream vehicles. A single transmission or suspension repair on these models can exceed the total plan premium.

How do I avoid extended warranty scams?

Legitimate providers never cold-call consumers and always provide a sample contract before payment. Verify any provider through the Better Business Bureau and FTC records before signing.

Is an extended warranty the same as insurance?

Extended warranties are legally classified as service contracts, not insurance, in most states. California is an exception, where these products must be sold by licensed insurance providers.

What does extended insurance typically cover?

Coverage depends on the plan tier. Powertrain plans cover the engine, transmission, and drivetrain. Bumper-to-bumper or comprehensive plans also cover electrical systems, cooling systems, and high-tech components. Always read the definitions section to confirm what qualifies as a covered component under your specific contract.