TL;DR:

- Vehicle protection budgeting involves planning for maintenance, insurance, warranties, and physical safeguards. Owners often underestimate costs by focusing only on basic expenses and neglecting vehicle-specific factors. Prioritizing these categories and adjusting for your vehicle's make, model, and mileage ensures a prepared and cost-effective protection plan.

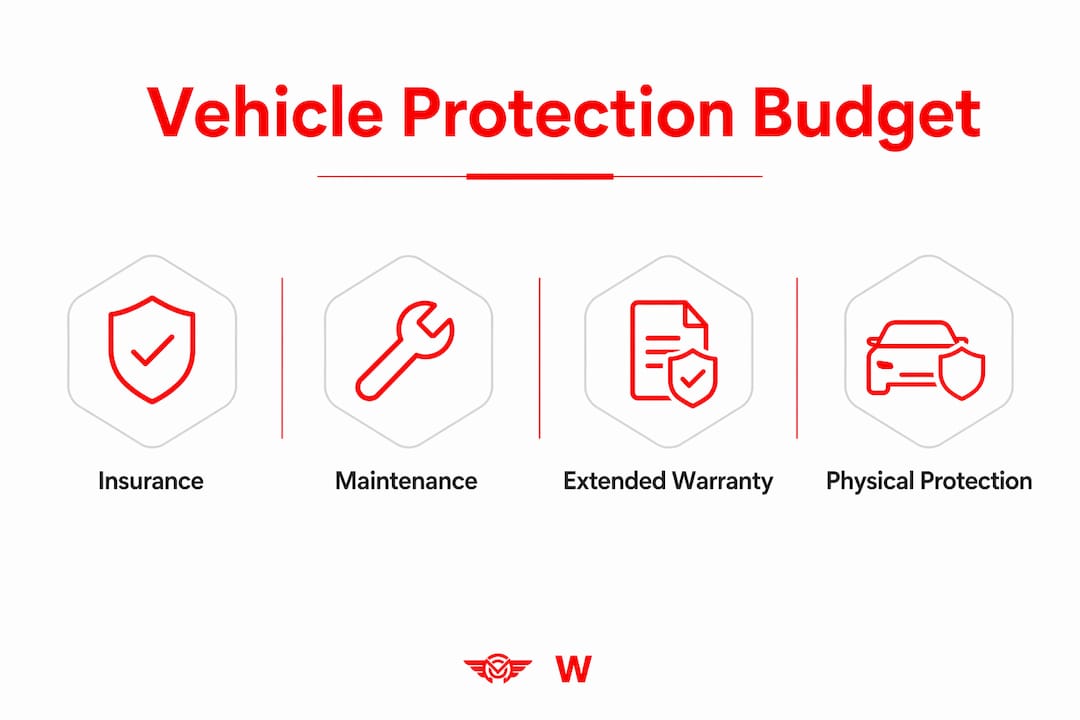

Budgeting for vehicle protection means allocating funds across four core areas: routine maintenance, auto insurance, extended warranties, and physical protection services. Most vehicle owners underestimate total annual costs because they plan for oil changes but ignore the larger picture. A BMW 5 Series, a Ford F-150, and a Honda Accord each carry different cost profiles, so a one-size-fits-all number fails every owner. Knowing how to budget for vehicle protection by category gives you a clear, workable plan instead of a surprise bill.

What are the main components to include in a vehicle protection budget?

A complete vehicle protection budget covers four distinct cost categories. Treating them separately makes it easier to prioritize and adjust as your financial situation changes.

Routine maintenance

Routine service costs range from $95 to $237 for standard visits and $296 to $474 for major services. Owners should budget $400 to $1,200 annually for routine maintenance depending on vehicle age and type. A Range Rover or Mercedes will sit at the top of that range because parts and labor rates are higher. A Honda Civic or Ford Focus typically lands near the bottom.

Auto insurance premiums

Average annual auto insurance premiums in 2026 run approximately $2,290, with minimum coverage plans averaging $1,562 and full coverage averaging $2,920. That spread means your coverage choice directly shapes your monthly budget. A Porsche 911 or Mercedes G-Class will push premiums toward the top of the full-coverage range because repair costs are higher.

Extended warranties

Extended warranties are a misunderstood budget item. Dealer sticker prices for extended warranties often reach $2,000, but real-world typical values average $1,200 to $1,400. That gap is money left on the table if you accept the first number presented. Buying through a third-party provider like Rpmwarranty gives you plan options at prices that reflect actual coverage value.

Physical protection services

Paint protection film, ceramic window tinting, and anti-theft devices round out the budget. Ceramic window tinting reduces cabin temperature by 20 to 25°F and blocks 99% of UV rays. It is typically the least expensive physical protection service, making it a strong first investment. Paint protection film for a full vehicle costs more but protects the finish of a Porsche Cayenne or BMW X5 from road debris that would otherwise mean expensive repaints.

| Category | Typical Annual Cost | Notes |

|---|---|---|

| Routine maintenance | $400–$1,200 | Higher for luxury and high-tech vehicles |

| Auto insurance | $1,562–$2,920 | Varies by coverage level and vehicle model |

| Extended warranty | $1,200–$1,400 | Dealer sticker often inflated to $2,000+ |

| Window tinting | $200–$500 | Strong UV protection, low entry cost |

| Paint protection film | $500–$2,500+ | Partial front-end kit offers best ROI |

| Anti-theft devices | $100–$400 | Can reduce insurance premiums |

Pro Tip: Research your specific make and model on owner forums before budgeting. BMW and Mercedes owners consistently report higher parts costs than generic estimates suggest, so real-world data from other owners beats any average.

How to estimate and plan monthly savings based on mileage and vehicle model

Calculating your monthly savings target starts with a simple baseline and then adjusts for your specific vehicle.

-

Start with the per-mile baseline. The standard estimate is $0.11 per mile for average vehicle maintenance. At 15,000 miles per year, that equals roughly $1,650 annually, or about $138 per month. This covers oil changes, filters, brakes, and tires across a typical ownership cycle.

-

Adjust for your vehicle brand and age. A Ford F-150 with 40,000 miles behaves differently than a BMW 7 Series with the same mileage. Modern vehicles, especially EVs and hybrids, carry higher labor and parts costs that reshape the $0.11 baseline upward. A BMW owner should realistically plan for $0.15 to $0.18 per mile. A Honda Accord owner can stay closer to the baseline.

-

Add a repair cushion. A 10 to 20% buffer on top of mileage-based estimates covers unpredictable component failures. For a $1,650 annual estimate, that means setting aside an extra $165 to $330 per year. Older vehicles and high-tech vehicles need the full 20% because failure costs spike without warning.

-

Identify known upcoming expenses. If your tires are due in six months and a brake job is coming at the next service, calculate those costs now and divide them across the months remaining. A set of tires for a Range Rover Sport can run $1,200 to $1,600. Spreading that cost over six months adds $200 to $267 to your monthly savings target.

-

Set your monthly savings number. Add your per-mile estimate, your repair cushion, and your spread upcoming costs. Divide the total by 12. That number is your monthly vehicle maintenance savings target. Keep it in a dedicated savings account separate from daily spending.

-

Example for a BMW 3 Series owner. At 12,000 miles per year and $0.16 per mile, the base estimate is $1,920. Adding a 15% cushion brings the total to $2,208. Dividing by 12 gives a monthly savings target of $184. That number is specific, defensible, and adjustable.

Pro Tip: Track every actual repair and maintenance expense in a simple spreadsheet. Review it each january and adjust your monthly savings target. Most owners find their real costs differ from estimates by 15 to 25% in the first year.

How to balance insurance coverage and deductible choices to optimize budget and protection

Insurance is the largest single line item in most vehicle protection budgets. Getting the balance right between coverage level and deductible size saves real money without leaving you exposed.

Higher deductibles reduce monthly premiums but require you to cover more out of pocket when a claim happens. A $1,000 deductible lowers your monthly bill meaningfully, but only makes financial sense if you have that $1,000 available in an emergency fund. Choosing a high deductible without the savings to back it up is a false economy. Financial experts are clear: build the emergency fund first, then raise the deductible.

Continuous coverage saves approximately 11% compared to letting your policy lapse and restarting. That saving compounds over years of ownership. Owners who drop coverage during a slow financial period pay more when they restart, which erases any short-term savings.

Key strategies for optimizing your insurance budget:

- Match coverage level to vehicle value. A 12-year-old Ford Focus does not need the same full-coverage policy as a new Mercedes E-Class. As a vehicle depreciates, dropping from full coverage to liability-only can free up $100 or more per month.

- Leverage safety feature discounts. Vehicles with top IIHS safety ratings and installed anti-theft devices qualify for discounts at most major insurers. A Honda CR-V or Ford Explorer with a factory alarm and strong crash ratings can earn meaningful reductions.

- Bundle policies. Combining home and auto insurance with one carrier typically produces a discount. This is one of the fastest ways to reduce the insurance line in your budget.

- Review your policy annually. Vehicle value drops every year. Your coverage limits and deductibles should reflect current value, not the price you paid three years ago.

- Ask about mileage-based programs. Low-mileage drivers who use their Porsche or BMW on weekends rather than daily commutes often qualify for usage-based insurance programs that reduce premiums significantly.

Prioritizing physical vehicle protection: what to invest in first based on budget

Physical protection is the category most owners either skip entirely or overspend on without a clear plan. A tiered approach solves both problems.

Phased investment in paint protection starts with the highest-impact areas: the front bumper, hood, and fender edges. These panels absorb the most road debris and are the most expensive to repaint. A partial front-end paint protection film kit delivers the best return on investment before you commit to full-vehicle coverage. For a Mercedes C-Class or Porsche Macan, avoiding a single front-bumper repaint more than pays for the film.

Ceramic window tinting is the right first step for most budgets. The cost is low, the UV protection is immediate, and the cabin comfort benefit is measurable. After tinting, move to front-end paint protection film, then expand coverage as your budget allows.

Dealer sticker prices for paint protection often reach $900, while the real market value sits between $300 and $400. Aftermarket installers with strong reviews consistently deliver the same or better quality at lower prices. For a BMW M4 or Range Rover Velar, the finish quality of the protection matters as much as the coverage area, so choose an installer with documented experience on luxury vehicles.

| Protection type | Coverage extent | Typical cost | Best for |

|---|---|---|---|

| Ceramic window tint | All windows | $200–$500 | All vehicles, first investment |

| Partial paint film | Front bumper, hood, fenders | $500–$900 | High-value vehicles, budget-conscious owners |

| Full paint film | Entire vehicle | $1,500–$2,500+ | Luxury vehicles, long-term ownership |

| Anti-theft alarm | Vehicle-wide | $100–$400 | All vehicles, insurance discount eligible |

Pro Tip: Avoid buying physical protection packages at the dealership on delivery day. You are under time pressure, and dealer markups on these services are consistently the highest. Schedule the work separately with a specialist installer after you have had time to compare prices.

Key Takeaways

Effective vehicle protection budgeting requires splitting costs across maintenance, insurance, warranties, and physical protection, then adjusting each category for your specific vehicle make, model, and mileage.

| Point | Details |

|---|---|

| Use a per-mile baseline | Budget $0.11 per mile as a starting point, then adjust upward for luxury or high-tech vehicles. |

| Add a repair cushion | Set aside 10–20% above your mileage estimate to cover unexpected component failures. |

| Match insurance to vehicle value | Adjust coverage levels and deductibles annually as your vehicle depreciates. |

| Invest in physical protection in phases | Start with window tinting and front-end paint film before committing to full-vehicle coverage. |

| Avoid dealer sticker prices | Extended warranties and paint protection cost significantly less through third-party providers. |

What I've learned about vehicle protection budgets after years of watching owners get it wrong

The most common mistake I see is treating vehicle protection as a single purchase rather than an ongoing financial category. Owners buy a car, pay for the dealer's protection package on day one, and then mentally close the file. Two years later, they are hit with a $1,800 transmission repair on their BMW X3 that no one planned for, because the budget never included a repair cushion.

The second mistake is buying protection in the wrong order. Full-body paint protection film on a new Ford Mustang sounds appealing, but if you have not sorted your insurance deductible or built an emergency fund, you have spent $2,000 protecting the paint while leaving yourself exposed to a $5,000 mechanical repair bill.

My practical recommendation is to build the budget in layers. Start with insurance and an emergency fund. Add routine maintenance savings with a 15% cushion. Then, once those foundations are solid, invest in physical protection starting with the highest-impact, lowest-cost items. Window tinting and front-end film on a Mercedes GLE or Porsche Cayenne protect real money without requiring a large upfront commitment.

Vehicle-specific research matters more than any generic average. A Honda Pilot owner and a Range Rover Sport owner are not working from the same numbers. Owner forums, independent repair shop estimates, and model-specific maintenance schedules give you data that generic calculators cannot. Rebalance your budget every january using actual expenses from the prior year. The owners who do this consistently are never surprised by a repair bill.

— Kenneth

Rpmwarranty's protection plans for every budget

Vehicle protection planning works best when your extended warranty matches your vehicle and your budget, not a dealer's margin target.

Rpmwarranty offers tiered protection plans covering engines, transmissions, cooling systems, electrical systems, and high-tech components across a wide range of makes and models. The Elite, Advanced, and Essential plans give owners the flexibility to match coverage depth to their actual financial situation. Whether you drive a BMW, Ford, Honda, or a specialty vehicle, Rpmwarranty's four-step process, from consultation through final agreement, makes it straightforward to find a plan that fits. Get a free quote and compare coverage options at Rpmwarranty.com.

FAQ

How much should I budget annually for vehicle protection?

Most owners need $2,000 to $5,500 per year when combining routine maintenance, insurance, an extended warranty, and physical protection. The exact number depends on vehicle make, model, age, and coverage choices.

What is the $0.11 per mile rule for vehicle maintenance?

The $0.11 per mile baseline is a standard estimate for average vehicle maintenance costs. At 15,000 miles per year, it produces roughly $1,650 annually, though luxury and high-tech vehicles typically require a higher per-mile figure.

Should I choose a higher deductible to save on insurance premiums?

A higher deductible lowers your monthly premium but only makes financial sense if you have an emergency fund large enough to cover that deductible out of pocket. Build the emergency fund first, then raise the deductible.

Is paint protection film worth the cost on a luxury vehicle?

For vehicles like a Porsche Macan or Mercedes C-Class, a partial front-end paint protection film kit delivers strong return on investment by preventing costly bumper and hood repaints. Start with front-end coverage before committing to full-vehicle film.

How do I avoid overpaying for an extended warranty?

Extended warranty dealer sticker prices average $2,000, while real-world market values run $1,200 to $1,400. Buying through a third-party provider and comparing plan options against your vehicle's specific coverage needs consistently produces better value than accepting the dealer's first offer.