TL;DR:

- Gap coverage is an essential add-on that pays the difference between your car’s depreciation-adjusted value and remaining loan balance after a total loss. It protects drivers from significant out-of-pocket expenses when insurance payouts fall short of their loan obligations, especially during the vehicle's early years of rapid depreciation. Purchasing gap insurance from your auto insurer is more cost-effective and offers smoother claims processing than dealer or lender options, and canceling it once your loan balance drops below your vehicle's value maximizes your benefit.

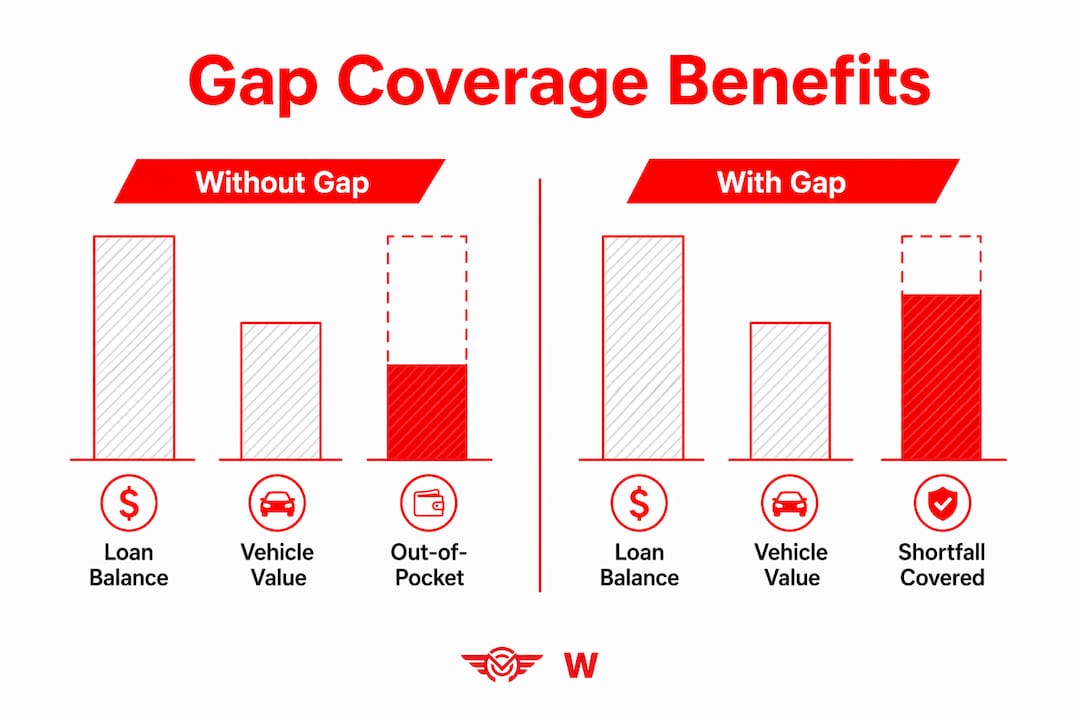

Gap coverage is defined as the insurance add-on that pays the difference between your car's depreciated actual cash value and the remaining balance on your loan or lease after a total loss or theft. Most drivers assume their standard auto policy covers everything. It does not. When your vehicle is totaled, your insurer pays what the car is worth today, not what you still owe the bank. That gap can run into thousands of dollars, and without protection, you pay it out of pocket. Understanding why gap coverage matters is the first step toward making a financially sound decision when financing or leasing a vehicle.

Why the importance of gap coverage is greater than most drivers realize

Standard comprehensive and collision insurance pays the actual cash value at the time of a total loss, not the loan payoff amount. This distinction is the core of why gap coverage exists. A vehicle worth $22,000 today with a $27,000 loan balance leaves a $5,000 shortfall that your primary insurer will not touch.

Full coverage insurance does not cover the remaining loan balance after a total loss. Many drivers believe "full coverage" means total financial protection. It means comprehensive and collision are included. The loan balance is a separate obligation entirely, and gap insurance is the only product designed to address it.

Resources like Kelley Blue Book and NADA Guides track vehicle depreciation in real time, and the numbers are sobering. A new BMW 5 Series or Mercedes-Benz C-Class can lose 15% to 20% of its value within the first twelve months. If you financed that vehicle with a small down payment and a 72-month loan, your loan balance will outpace the car's market value for a significant stretch of time.

Gap coverage is a critical financial safeguard when loan balances exceed vehicle value, protecting consumers from significant out-of-pocket expenses. The protection is not expensive relative to the risk it eliminates, which makes it one of the most cost-efficient add-ons available to financed vehicle owners.

How does gap insurance work with standard auto coverage?

Gap insurance functions as a secondary layer that activates only after your primary insurer settles a total loss or theft claim. The claim settlement sequence matters, and understanding it prevents confusion when you actually need to file.

Here is how the process works from start to finish:

- Total loss or theft occurs. Your comprehensive or collision coverage triggers a claim with your primary insurer.

- Primary insurer pays actual cash value. The insurer determines the vehicle's market value at the time of loss using tools like Kelley Blue Book and issues a check to your lender for that amount.

- Remaining loan balance is calculated. Your lender applies the ACV payment to your outstanding balance and identifies the shortfall.

- Gap coverage pays the difference. Your gap insurer pays the remaining balance directly to the lender, clearing your obligation.

- You walk away without residual debt. Without gap coverage, step four does not happen and you owe the shortfall personally.

One important detail: gap coverage pays after the insurer settles the ACV claim and does not cover your deductible. If your policy carries a $1,000 deductible, that amount comes out of your pocket regardless. Some gap products do cover deductibles, so comparing policy details before purchasing is worth the time.

Pro Tip: Check whether your gap policy includes deductible coverage before signing. Policies that absorb your deductible can save you an additional $500 to $1,000 at the worst possible moment.

Consider a practical example. You finance a new Honda Accord for $35,000 with $2,000 down on a 72-month loan. Eighteen months later, a collision totals the car. Kelley Blue Book values it at $26,500. Your insurer pays $26,500 to your lender. Your remaining loan balance is $31,200. Without gap coverage, you owe $4,700 on a car you no longer own. With gap coverage, that balance disappears.

Why gap coverage matters most in the first few years

The financial risk that gap coverage addresses is not constant across the life of a loan. It peaks in the first two to three years and gradually diminishes as your loan balance falls closer to the vehicle's market value.

Vehicle depreciation is the driving force behind this risk window:

- New vehicles lose roughly 20% of their value in the first year of ownership.

- By year three, cumulative depreciation often reaches 40% to 50% of the original purchase price.

- Certain models, including some luxury sedans and full-size trucks, depreciate even faster in their early years.

- Loan amortization schedules front-load interest payments, meaning your principal balance drops slowly in the early months.

- A 72-month loan with less than 20% down creates the deepest and longest underwater window.

Some fast-depreciation vehicles lose more than 30% of their value in the first year alone, deepening the gap significantly. A Range Rover or BMW X5 financed at full sticker price with minimal down payment can leave an owner underwater by $8,000 to $12,000 within the first eighteen months. That is not a theoretical risk. It is a predictable outcome of combining rapid depreciation with slow principal reduction.

"The 'underwater' loan situation occurs mainly in the first two to three years due to rapid depreciation and slow principal reduction, and is most common when the down payment is less than 20%, the loan term is long, or the vehicle depreciates quickly." — MoneyGeek

Loan amortization schedules combined with rapid depreciation create a window where owners are underwater, and gap insurance is most valuable during this period. Once your loan balance drops below the vehicle's current market value, the gap no longer exists and the coverage becomes unnecessary. Monitoring this crossover point is how you decide when to cancel.

Who needs gap coverage and how to decide if it's right for you

Gap insurance is not a universal requirement, but certain financing conditions make it close to mandatory. The right question is not whether gap coverage exists but whether your specific situation creates meaningful financial exposure.

The clearest indicator is the relationship between your loan balance and your vehicle's current market value. Use Kelley Blue Book or NADA Guides to check your car's value, then compare it to your loan payoff amount from your lender's online portal. If the loan exceeds the value, you are underwater and gap coverage is worth carrying.

| Situation | Gap coverage recommended? |

|---|---|

| Leased vehicle | Yes. Lease contracts frequently mandate gap coverage or similar waivers. |

| Down payment under 20% | Yes. Loan balance will exceed value immediately after purchase. |

| Loan term of 60 months or longer | Yes. Slow principal reduction extends the underwater window. |

| High-depreciation vehicle (luxury SUV, electric vehicle) | Yes. Rapid value loss deepens the gap faster. |

| Loan balance already below vehicle value | No. The gap no longer exists; cancel and save the premium. |

Leased vehicles almost always require gap insurance because the lease payoff frequently exceeds vehicle value after a loss. Most lease contracts from Ford, BMW, Mercedes-Benz, and Porsche financial arms either include gap protection or require it as a condition of the agreement. Verify your lease contract before purchasing separately.

Pro Tip: Pull your loan payoff balance and your vehicle's Kelley Blue Book value every six months. The moment your value exceeds your balance, cancel your gap coverage and redirect that premium toward your deductible fund.

Gap insurance must be paired with comprehensive and collision coverage and is only available when you still owe money on the vehicle. If you own your car outright, gap coverage is not applicable. The product exists specifically for financed and leased vehicles.

Gap insurance purchase options: insurer vs. dealer or lender

Where you buy gap coverage affects both what you pay and how smoothly a claim gets processed. Two primary channels exist: your auto insurance provider and the dealership or lender at the time of financing. The differences between them are significant.

Gap insurance through insurers costs $50 to $150 per year, while dealer or lender options typically run $500 to $700 as a flat fee, often rolled into the loan and accruing interest over time. That flat fee sounds manageable until you calculate the total cost with interest on a 72-month loan. A $600 dealer gap product financed at 7% over six years costs closer to $850 in real terms.

The table below summarizes the key differences:

| Factor | Insurer-purchased gap | Dealer or lender gap |

|---|---|---|

| Typical annual cost | $50 to $150 per year | $500 to $700 flat fee |

| Interest implications | None | Financed into loan, accrues interest |

| Claims process | Coordinated with primary insurer | Separate process, potential conflicts |

| Cancellation flexibility | Cancel anytime, often with refund | Refund policies vary widely |

| Coverage start | Immediate upon policy addition | Tied to loan origination |

Insurer-purchased gap coverage results in a less complicated claims process compared to dealer or lender add-ons, with fewer payment conflicts and smoother lender settlement coordination. When your primary insurer and gap insurer are the same company or work within the same claims ecosystem, the settlement sequence described earlier moves faster and with less paperwork.

Key considerations when comparing your options:

- Verify whether your state allows insurers to offer gap coverage, as availability varies by state.

- Confirm the dealer's gap product is not duplicating coverage already included in your lease agreement.

- Ask specifically whether the gap policy covers your deductible, not just the loan shortfall.

- Check the cancellation and refund terms before signing anything at the dealership finance desk.

Choosing gap insurance through your auto insurer offers better cost efficiency and smoother claims handling than dealer or lender options in most cases. The annual premium model also means you stop paying the moment you cancel, unlike a financed flat fee that stays in your loan balance regardless.

Key takeaways

Gap coverage protects financed and leased vehicle owners from owing money on a car they no longer have, and the insurer-purchased version delivers the best combination of cost and claims efficiency.

| Point | Details |

|---|---|

| Gap coverage fills the loan shortfall | It pays the difference between your insurer's ACV payout and your remaining loan or lease balance. |

| Risk peaks in years one through three | Rapid depreciation and slow principal reduction create the deepest underwater window early in a loan. |

| Leases almost always require it | Most lease agreements from major manufacturers mandate gap coverage or include it automatically. |

| Insurer-purchased gap costs less | Annual premiums of $50 to $150 beat dealer flat fees of $500 to $700 that accrue loan interest. |

| Cancel when the gap closes | Once your loan balance falls below your vehicle's market value, gap coverage is no longer necessary. |

What I've learned after years of watching gap coverage save and cost people money

The most common misconception I encounter is the belief that "full coverage" means total financial protection. Drivers with comprehensive and collision on a financed BMW 3 Series or Ford F-150 genuinely believe they are covered for everything. They are not. Full coverage is an industry shorthand, not a legal guarantee that your loan balance disappears after a total loss.

The second thing I have observed is that people buy gap coverage at the dealership without comparing it to what their insurer offers. The finance manager presents it as a line item in a stack of paperwork, and most buyers sign without asking about the cost difference. Paying $600 financed into a loan versus $100 per year through your insurer is a $300 to $400 difference over three years. That is real money.

What I find genuinely underappreciated is the timing element. Gap coverage is not a permanent fixture. It is a temporary safeguard for a specific financial window. The drivers who benefit most are those who add it immediately after financing a high-depreciation vehicle like a Range Rover Sport or Mercedes-Benz GLE, carry it through the underwater period, and cancel it the moment their loan balance drops below market value. That disciplined approach captures the protection without overpaying for coverage you no longer need.

The cost-versus-benefit math is straightforward. A $5,000 to $10,000 loan shortfall after a total loss is a financial event that takes years to recover from. An annual premium of $100 to $150 is not. The asymmetry alone makes gap coverage one of the clearest financial decisions in vehicle ownership.

— Kenneth

Protect your vehicle with the right coverage from Rpmwarranty

Gap insurance handles the financial exposure at the front end of vehicle ownership, but your protection needs extend well beyond the loan payoff period. Once your loan balance and vehicle value align, the next risk is mechanical failure, and that is where an extended warranty becomes your most valuable asset. Rpmwarranty offers extended vehicle warranty plans trusted by dealers nationwide, covering engines, transmissions, electrical systems, and high-tech components across a wide range of makes and models. Whether you drive a Honda, Porsche, Ford, or BMW, Rpmwarranty's Elite, Advanced, and Essential plans give you a tailored layer of protection that keeps repair costs from derailing your finances long after the gap closes.

FAQ

What does gap insurance actually cover?

Gap insurance covers only the difference between your insurer's actual cash value payout and your remaining loan or lease balance after a total loss or theft. It does not cover repair costs, medical expenses, or your deductible unless the policy specifically includes deductible protection.

Does full coverage auto insurance include gap protection?

Full coverage does not include gap protection. Comprehensive and collision insurance pay the vehicle's actual cash value at the time of loss, which is almost always less than the outstanding loan balance in the first few years of ownership.

When should I cancel gap insurance?

Cancel gap insurance once your loan balance falls below your vehicle's current market value. Check your Kelley Blue Book value against your loan payoff amount every six months to identify when this crossover occurs.

Is gap insurance required for a leased vehicle?

Leased vehicles almost always require gap insurance, and many lease agreements from manufacturers like BMW, Mercedes-Benz, and Ford include it automatically or mandate it as a condition of the lease. Review your lease contract before purchasing a separate policy.

Where is the cheapest place to buy gap insurance?

Purchasing gap insurance through your auto insurer costs $50 to $150 per year, which is significantly less than the $500 to $700 flat fee charged by most dealerships and lenders, especially when that fee is financed into your loan and accrues interest over time.