TL;DR:

- Warranty insurance covers vehicle repairs after the factory warranty ends, reducing unexpected costs. It differs from car insurance, which protects against external damage, and requires proper documentation to ensure claim approval. Choosing the right plan depends on your vehicle's needs, maintenance record-keeping, and understanding your legal rights.

Warranty insurance is a service contract that covers the cost of mechanical or electrical repairs when your vehicle's factory warranty expires. The industry term for this product is an extended service contract, though "warranty insurance" is the phrase most vehicle owners search for. Manufacturer factory warranties last 3–5 years, and once that window closes, a single repair on a BMW 5 Series transmission or a Range Rover air suspension system can cost thousands of dollars out of pocket. Extended warranty coverage fills that gap by converting unpredictable repair bills into a fixed monthly or annual cost. Rpmwarranty offers tiered plans, including Elite, Advanced, and Essential, designed to match different vehicles, budgets, and risk profiles.

What is warranty insurance and how does it work?

Warranty insurance is a financial protection plan that pays for covered mechanical or electrical failures in your vehicle after the original factory warranty ends. It does not cover damage from accidents, weather, or theft. Those risks belong to your standard auto insurance policy. The two products are designed to work together, not replace each other.

Insurance-backed warranties transform a provider's repair promise into a financially secured obligation, which means you are protected even if the warranty company faces financial trouble. That backing is what separates a credible extended service contract from a paper promise. When you buy a plan from a financially backed provider, you are purchasing real coverage, not just a handshake agreement.

The coverage activates when a covered component fails due to a defect or normal wear. You contact your provider, verify that the repair falls within your plan, and the provider pays the shop directly or reimburses you after the repair. The exact process depends on your contract terms, but the core structure is consistent across the industry.

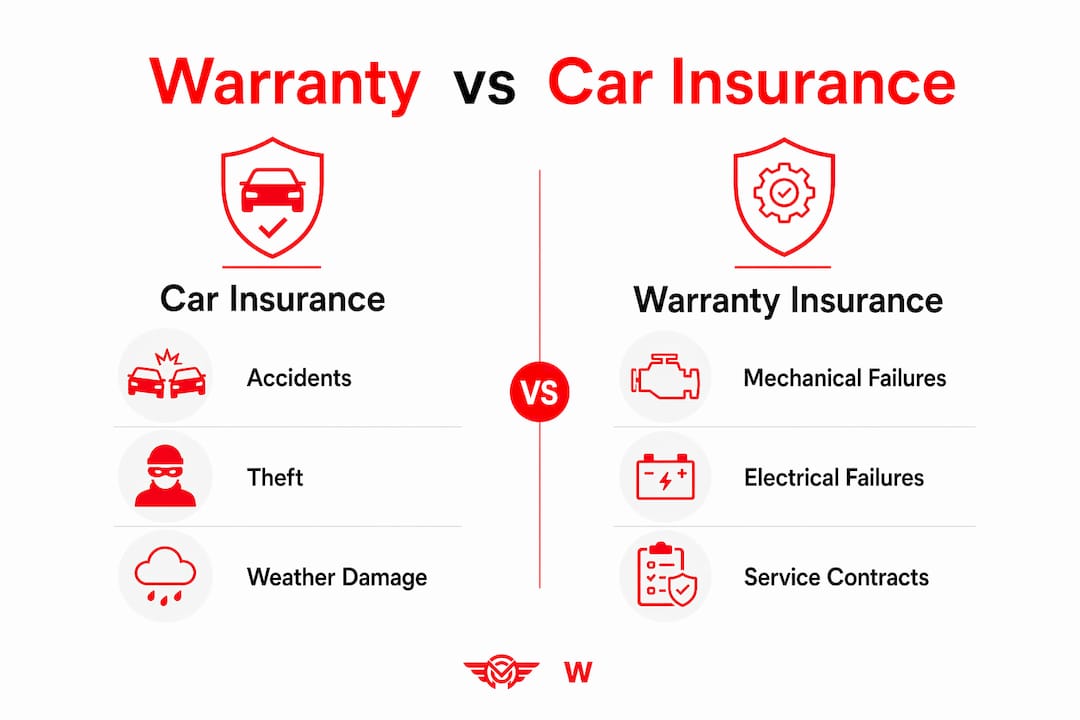

How does warranty insurance differ from traditional car insurance?

Car insurance covers external events like accidents, theft, and weather damage. Warranty coverage addresses internal mechanical and electrical failures caused by defects or wear. The legal distinction matters because the two products are regulated differently, priced differently, and triggered by completely different events.

A Mercedes-Benz C-Class owner who gets rear-ended files a claim with their auto insurer. The same owner whose transfer case fails at 80,000 miles files a claim with their warranty provider. Neither policy covers the other's territory. Confusing the two leads vehicle owners to skip extended coverage, assuming their auto policy will handle repair bills. It will not.

The table below shows the key differences at a glance.

| Category | Car insurance | Warranty insurance |

|---|---|---|

| What it covers | Accidents, theft, weather damage | Mechanical and electrical failures |

| What triggers a claim | External event or collision | Internal component failure or defect |

| Legal classification | Insurance product | Service contract |

| Typical annual cost | Varies by driver and vehicle | Varies by plan tier and vehicle age |

| Maintenance required | No | Yes, with documentation |

The cost difference is also significant. Extended warranties offset routine mechanical maintenance costs, while auto insurance covers disaster-related damage. For high-end vehicles like a Porsche Cayenne or a BMW X5, extended warranty costs are modest compared to the repair bills those vehicles generate after the factory warranty expires.

Pro Tip: Read both your auto insurance policy and your warranty contract before you need them. Knowing which product covers which failure saves you time and frustration when something breaks.

What coverage options and costs are typical for vehicle warranty insurance?

Coverage tiers vary by provider and plan, but most extended service contracts fall into three broad categories. Powertrain plans cover the engine, transmission, and drivetrain. Mid-level plans add electrical systems, cooling, and brakes. Comprehensive plans, sometimes called exclusionary plans, cover everything except a defined list of wear items.

Common coverage areas across most plans include:

- Engine components: pistons, crankshafts, camshafts, and seals

- Transmission: internal gears, torque converters, and clutch packs on automatics

- Cooling system: water pump, radiator, and thermostat housing

- Electrical systems: alternators, starters, and onboard control modules

- Brakes: master cylinder and calipers, but not pads or rotors

- High-tech components: navigation systems, backup cameras, and driver-assist modules on newer vehicles

Common warranty exclusions include wear-and-tear items such as brake pads, tires, and fluids. Those are your responsibility to maintain and replace on schedule. Failing to do so does not just cost you money on those items. It can void coverage on related components if a provider can show that neglect caused the failure.

Honda Accord owners typically face lower extended warranty costs than Range Rover Sport owners because repair frequency and parts costs differ significantly. A Ford F-150 powertrain plan costs less than a Mercedes-Benz GLE comprehensive plan. Vehicle age, mileage, and make all factor into pricing.

Deductibles on extended service contracts typically range from $0 to $200 per repair visit. A $0 deductible plan costs more upfront but reduces friction at the repair shop. A higher deductible lowers your monthly cost but means you pay more each time you file a claim.

Pro Tip: Keep every oil change receipt, tire rotation record, and fluid service invoice. Lack of documentation is the primary cause of warranty claim denial, and a complete service file is your strongest defense.

How does the warranty insurance claims process work?

Filing a warranty claim follows a clear sequence. Skipping steps or acting before your provider approves a repair is the fastest way to get a claim denied. Follow the process in order.

- Contact your provider first. Call or log in to your provider's claims line before authorizing any repair work. Describe the symptom, not just the part. Providers need to verify that the failure falls within your coverage before work begins.

- Take the vehicle to a qualified shop. Federal law allows warranty repairs at any qualified repair facility as long as repairs meet manufacturer specifications and are properly documented. You are not required to use a dealership.

- Allow the shop to diagnose the problem. The technician provides a written diagnosis and repair estimate. Your provider reviews this before approving the work. For straightforward repairs, approval is often immediate.

- Wait for authorization on complex repairs. Simple warranty claims often process instantly, but extended warranty claims on costly repairs may include inspections that delay approval by days or weeks. A BMW 7 Series engine replacement will take longer to approve than a Honda Civic alternator swap.

- Confirm payment terms. Some providers pay the shop directly. Others reimburse you after you pay. Know which method your contract uses before you authorize the repair.

If your claim is denied, request the denial in writing. The burden of proof lies on the manufacturer or dealer to justify a denial with specific documentation. A denial based on vague reasoning is challengeable. Gather your service records, the shop's diagnosis, and any correspondence, then submit a formal appeal.

Pro Tip: Ask the repair shop to note the mileage, date, and specific failure code on every invoice. That detail strengthens your claim file and makes appeals much easier if a dispute arises.

What legal protections and consumer rights exist for warranty insurance customers?

Federal law gives vehicle owners more power than most realize. Dealers and manufacturers cannot refuse warranty work simply because repairs were done at an independent certified shop. Dealerships may prefer to perform warranty work themselves for financial reasons, but preference does not override your legal rights.

The Magnuson-Moss Warranty Act is the primary federal law governing written warranties on consumer products, including vehicles. It requires warranty terms to be clear and available before purchase. It also limits the conditions a manufacturer can place on warranty coverage. A dealer cannot void your warranty because you used a non-dealer oil change service, for example, unless they can prove that service caused the specific failure.

Consumers are legally protected to use independent mechanics as long as repairs meet warranty standards and are documented properly. Receipts from reputable independent shops or detailed service logs are legally sufficient proof of maintenance compliance. That matters for Porsche and BMW owners who prefer independent specialists over dealership service departments.

The table below outlines common exclusion categories and the consumer rights that apply.

| Exclusion category | Why it is excluded | Your right |

|---|---|---|

| Brake pads and rotors | Normal wear items | Maintain and document replacement |

| Tires | Wear and road hazard | Covered by separate tire protection |

| Fluids and filters | Routine maintenance | Keep receipts as proof of service |

| Pre-existing conditions | Failure existed before coverage | Dispute with inspection evidence |

| Damage from neglect | Owner responsibility | Prove maintenance with service records |

State laws add another layer of protection in many cases. Some states require extended warranty providers to maintain financial reserves or post bonds, which protects you if the company closes. Checking your state's insurance department website confirms what protections apply in your location.

How to choose the best warranty insurance coverage for your vehicle?

The right plan depends on your vehicle, your driving habits, and your financial tolerance for repair risk. A one-size-fits-all approach leads to either overpaying for coverage you do not need or underbuying and facing gaps when something expensive fails.

Start by assessing your vehicle's known weak points. Range Rover air suspension systems are expensive to repair. BMW N63 engines have documented cooling issues. Mercedes-Benz AIRMATIC suspension components carry high parts costs. Ford F-150 EcoBoost engines are generally reliable but can develop turbo issues at higher mileage. Knowing your vehicle's history tells you which coverage tier makes financial sense.

Key factors to evaluate when selecting a plan:

- Coverage length: Match the plan term to how long you plan to keep the vehicle. A three-year plan on a vehicle you plan to sell in two years wastes money.

- Deductible structure: A $0 deductible suits owners who want zero friction at the shop. A $100 or $200 deductible lowers the plan cost for owners who rarely need repairs.

- Exclusion list: Read it carefully. A plan that excludes your vehicle's most failure-prone components is not a good plan regardless of price.

- Claims service quality: A provider that delays approvals or disputes every claim costs you time and stress. Look for clear claims processes and direct shop payment.

- Provider financial backing: Confirm the provider carries financial reserves or insurance backing. Insurance-backed service contracts protect you if the company becomes insolvent.

- Maintenance requirements: Understand what the contract requires you to document. Failing to meet those requirements voids coverage.

Rpmwarranty's Elite, Advanced, and Essential plans address different points on this spectrum. Elite covers the widest range of components, including electrical and high-tech systems. Advanced covers powertrain and major mechanical systems. Essential focuses on core powertrain protection for owners who want basic coverage at a lower cost. Getting a free warranty quote takes minutes and gives you a concrete number to evaluate.

Key Takeaways

Warranty insurance is a service contract that protects vehicle owners from costly mechanical and electrical repair bills after the factory warranty expires, and maintaining complete service records is the single most effective way to keep that coverage valid.

| Point | Details |

|---|---|

| Warranty vs. car insurance | Warranty covers internal mechanical failures; car insurance covers external damage like accidents and theft. |

| Factory warranty limits | Manufacturer warranties last 3–5 years, leaving most vehicles unprotected for the majority of their useful life. |

| Documentation is critical | Lack of service records is the leading cause of claim denial; keep every receipt and invoice. |

| Legal rights matter | Federal law protects your right to use independent repair shops without losing warranty coverage. |

| Plan selection | Match coverage tier, deductible, and exclusion list to your specific vehicle's known failure points. |

What I have learned after years of watching warranty claims go wrong

The biggest mistake vehicle owners make is treating warranty coverage like a set-it-and-forget-it product. They buy the plan, file it away, and then discover at the worst possible moment that a claim is denied because they cannot prove they changed the oil on schedule.

I have seen BMW X5 owners lose coverage on a $4,000 transfer case repair because they could not produce three years of oil change records. The repair itself was clearly covered. The documentation gap was the problem. That is a painful and entirely avoidable outcome.

The second misunderstanding I see constantly is the belief that you must use a dealership for all service to keep your warranty valid. That is not true. Federal law allows repairs at any qualified facility as long as the work meets manufacturer specifications and is documented. A trusted independent shop that specializes in European vehicles often does better work than a high-volume dealership service department. Use whoever you trust, but get the paperwork every single time.

The third issue is underbuying coverage to save money upfront. A powertrain-only plan on a Range Rover Sport sounds affordable until the air suspension fails and you discover that system is not covered. The repair costs more than a year of comprehensive coverage would have. Match the plan to the vehicle, not to the lowest monthly payment.

My honest advice is this: treat your service records as financial documents. Store them the same way you store tax returns. When you file a claim, that file is your evidence. A complete maintenance history is not just good practice. It is the difference between an approved claim and a denied one.

— Kenneth

How Rpmwarranty protects your vehicle investment

Vehicle repairs are expensive, and the cost only rises as vehicles add more technology. Rpmwarranty provides extended vehicle warranty plans trusted by dealers nationwide, covering engines, transmissions, electrical systems, cooling systems, and high-tech components across a wide range of makes and models.

The four-step process, consultation, plan selection, customization, and final agreement, is built for clarity. You choose the coverage tier that fits your vehicle and budget, not a generic plan designed for someone else's car. Rpmwarranty's claims support team works directly with repair shops to keep approvals moving. Whether you drive a Honda Accord, a Porsche Cayenne, or a BMW 5 Series, there is a plan built around your vehicle's specific needs. Get your no-cost quote today and know exactly what your coverage costs before you need it.

FAQ

What is warranty insurance for a vehicle?

Warranty insurance, formally called an extended service contract, covers the cost of mechanical or electrical repairs after your factory warranty expires. It does not cover accident damage or theft.

What is the difference between insurance and warranty coverage?

Car insurance covers external damage from accidents, weather, and theft. Warranty coverage pays for internal mechanical or electrical failures caused by defects or normal wear.

How do warranty insurance claims work?

Contact your provider before authorizing any repair, allow the shop to diagnose the problem, and wait for provider approval. Simple claims process instantly, while complex repairs may require an inspection before approval.

Can a dealer refuse to do warranty work if I use an independent shop?

No. Federal law prohibits dealers from denying warranty claims solely because an independent certified shop performed prior repairs, as long as the work is documented and meets manufacturer specifications.

What voids a vehicle warranty insurance plan?

Failure to maintain required services with proper documentation is the most common reason for claim denial. Missing oil changes, skipping scheduled services, or lacking receipts to prove maintenance all put your coverage at risk.