TL;DR:

- Essential health plans cover ten core benefits mandated by law, including hospital, prescription, and mental health services. They also provide adult dental, vision, and wellness perks like OTC allowances with no premiums or deductibles for income-qualified individuals. Continuous enrollment and activation of benefits maximize value, making these plans an affordable and comprehensive protection option.

Essential plans are health insurance programs that include a mandated set of ten core benefits required by the Affordable Care Act, covering everything from hospital care and prescription drugs to mental health services and maternity care. Understanding what is covered in essential plans matters whether you are selecting health coverage or applying the same logic to any protection plan you buy. The New York Essential Plan, offered through providers like MetroPlusHealth, EmblemHealth, and Molina Healthcare, delivers this coverage with no monthly premiums or deductibles for eligible members. That combination of broad coverage and low cost makes essential plans one of the most misunderstood yet valuable options available to income-qualified individuals.

What is covered in essential plans: the 10 core benefits

The ten essential health benefits are the legal backbone of every essential plan. Federal law requires every qualifying plan to cover all ten categories without exception. Here is what each one means in practice:

- Outpatient care: Doctor visits, urgent care, and services you receive without being admitted to a hospital. This covers the routine checkups and sick visits most people use most often.

- Inpatient hospital care: Overnight stays, surgeries, and intensive treatment inside a hospital facility. If you are ever in a serious car accident driving a BMW 5 Series or a Ford F-150, this benefit covers the hospital admission that follows.

- Emergency services: Emergency room visits are covered even if the hospital is out of network. This protection applies regardless of how the emergency started.

- Maternity and newborn care: Prenatal visits, labor, delivery, and postnatal care for both mother and newborn. This coverage begins before birth and continues after.

- Mental health and substance use services: Therapy, psychiatric care, and treatment for addiction. These services receive the same coverage level as physical health services under federal parity rules.

- Prescription drugs: A defined formulary of covered medications, from generic antibiotics to specialty drugs. Copays vary by drug tier and plan variant.

- Rehabilitative and habilitative services: Physical therapy, occupational therapy, and speech therapy. Habilitative services help people develop skills they never had, while rehabilitative services restore skills lost to injury or illness.

- Lab tests and diagnostic imaging: Blood work, X-rays, MRIs, and other diagnostic services ordered by your provider. These are covered when medically necessary.

- Preventive and wellness services: 100% free preventive care including cancer screenings, diabetes checks, blood pressure monitoring, and immunizations. You pay nothing for these services.

- Pediatric services: Dental and vision care for children under 19, plus routine pediatric checkups. Adult dental and vision are handled separately, which we cover in the next section.

The preventive care benefit deserves special attention. Free screenings and immunizations are not just a perk. They are the single most cost-effective benefit in the plan because catching a condition early costs far less than treating it late.

How do essential plans cover dental, vision, and wellness?

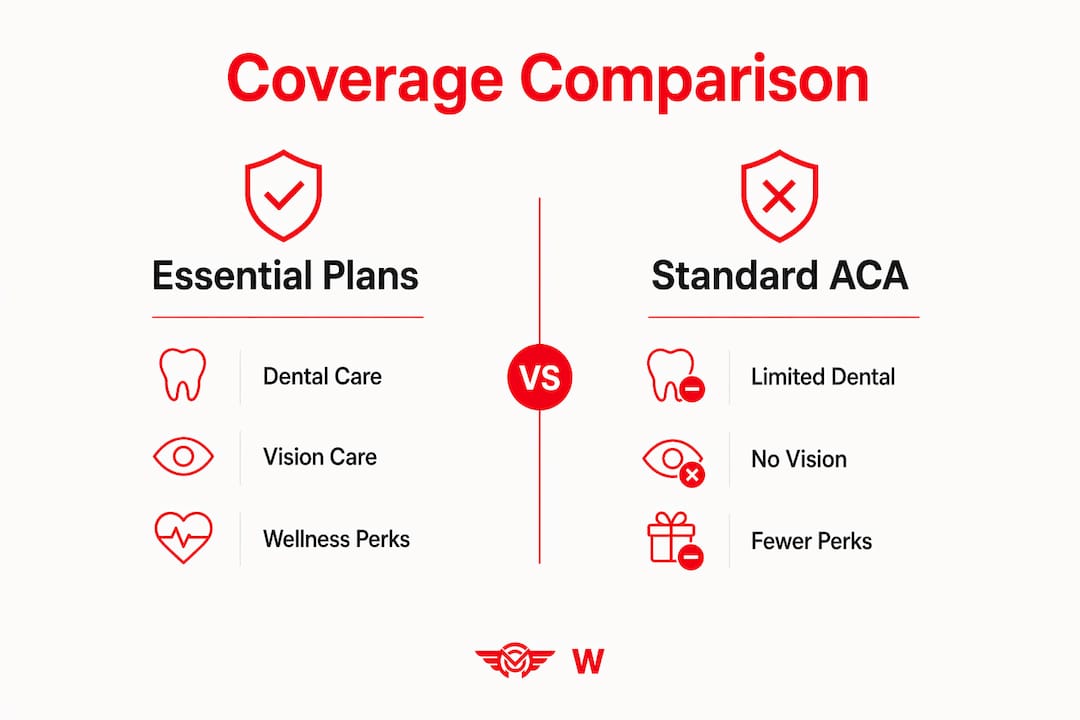

Standard ACA benchmark plans frequently exclude routine adult dental and vision care. Essential plans break from that pattern in a meaningful way. Adult dental and vision benefits are included as standard coverage, not add-ons you pay extra for.

Dental coverage details

The dental benefit covers one routine oral exam per year, one professional cleaning, and one set of dental X-rays annually. Tooth extractions are also covered when necessary. This is not comprehensive dental insurance covering crowns and implants, but it handles the preventive and basic restorative care that keeps most adults out of serious dental trouble.

Vision coverage details

The vision benefit includes one annual eye exam and coverage for either prescription glasses or contact lenses per year. For anyone who wears corrective lenses, this benefit alone represents hundreds of dollars in annual savings.

Wellness perks that most members miss

Beyond dental and vision, essential plans offered by providers like MetroPlusHealth include quarterly OTC spending allowances, gym membership reimbursements, and grocery store benefits. These extras require active enrollment or use of a member rewards card. Most members never claim them simply because they do not know they exist.

| Benefit Category | Essential Plan Coverage | Standard ACA Benchmark Plan |

|---|---|---|

| Adult Dental | Exam, cleaning, X-ray, extractions | Not typically included |

| Adult Vision | Annual exam, glasses or contacts | Not typically included |

| Preventive Care | 100% free | 100% free |

| OTC Allowance | Quarterly spending card (varies by plan) | Not included |

| Gym Reimbursement | Available through member rewards | Not included |

| Grocery Benefits | Available through member rewards | Not included |

Pro Tip: Activate your member rewards card the day you enroll. Gym reimbursements and OTC allowances expire if unused within the quarter, and most members forfeit this money simply by forgetting to register.

Who qualifies for essential plans and what affects eligibility?

Essential plan eligibility is defined by income, age, and residency status. The New York Essential Plan serves adults between ages 19 and 64 who earn up to 250% of the federal poverty level. Income limits set the threshold at $39,125 per year for a single-person household and $80,375 for a household of five, with each additional person above five adding $10,760 to the limit.

Legal residency is required, but the definition is broader than many people assume. DACA recipients and certain immigrants qualify for the Essential Plan, which is a distinct program from Medicaid. The Essential Plan serves people who earn too much for Medicaid but still need affordable coverage.

How plan variants work

Essential plans come in variants, typically labeled Plan 1 through Plan 4, based on income bracket. Core medical coverage stays consistent across all variants. What changes is the cost-sharing structure and access to supplemental perks.

- Plan 1: Lowest income bracket, $0 premiums, lowest copays, maximum supplemental benefits including OTC allowances and transportation assistance.

- Plan 2: Slightly higher income, still $0 or very low premiums, moderate copays, access to most supplemental perks.

- Plan 3 and Plan 4: Higher income brackets within the 250% FPL ceiling, modest premiums in some cases, higher copays, reduced supplemental extras.

Income brackets strongly influence which supplemental benefits you receive, even though your core medical coverage remains the same. This is the detail most applicants miss when comparing variants.

Enrollment timing

Essential plans allow continuous enrollment year-round, not just during open enrollment periods. If you lose employer-sponsored insurance mid-year, you can apply immediately rather than waiting months for an open enrollment window. That flexibility is a practical advantage most people do not realize they have until they need it.

What are the out-of-pocket costs in essential plans?

Essential plans are built to minimize financial barriers. Most members pay $0 in premiums and face no deductible, meaning coverage kicks in from the first dollar of care. Preventive services are always free regardless of plan variant.

Copayments apply to most other services, and the amounts depend on your plan variant and the type of care:

- Primary care visits: Low fixed copay, typically in the range of $0 to $15 depending on variant.

- Specialist visits: Slightly higher copay, often $25 or less for Plan 1 and Plan 2 members.

- Emergency room visits: Higher copay, but waived if you are admitted to the hospital.

- Prescription drugs: Tiered copays based on drug category. Generic drugs carry the lowest copays. Specialty drugs carry the highest, though still capped.

- Mental health visits: Covered at the same copay level as primary care under federal parity rules.

The absence of a deductible is the most financially significant feature of these plans. With a traditional marketplace plan, you might pay the first $1,500 to $7,000 out of pocket before insurance contributes anything. Essential plans eliminate that barrier entirely.

Pro Tip: Always verify that your preferred doctors and specialists are in-network before your first appointment. Staying in-network is the single most effective way to avoid surprise bills, since out-of-network care is not covered except in true emergencies.

How car owners can apply essential plan thinking to warranty coverage

The logic behind essential plan coverage translates directly to vehicle warranty decisions. Both types of protection share the same structure: a defined set of core covered items, optional supplemental benefits, cost-sharing through copays or deductibles, and network restrictions that determine where you can get service.

When you evaluate a vehicle warranty plan, apply the same scrutiny you would to a health plan:

- Identify the core coverage: What components does the plan cover? For a BMW 3 Series or a Mercedes-Benz C-Class, you want to confirm that the engine, transmission, cooling system, and electrical components are all explicitly listed. Vague language like "major components" is the warranty equivalent of an incomplete benefits summary.

- Look for supplemental perks: Roadside assistance, rental car reimbursement, and trip interruption coverage are the warranty world's equivalent of dental and vision benefits. They are not always included in base plans, but they deliver real value when you need them.

- Understand cost-sharing: Deductibles and copays exist in warranty plans too. A plan with a $0 deductible costs more upfront but saves money when repairs happen. A higher deductible lowers your monthly cost but increases your exposure on each claim.

- Check the service network: Just as essential plan members must use in-network providers to avoid surprise costs, warranty holders must use authorized repair facilities. A Range Rover or Porsche Cayenne owner needs to confirm that their preferred dealership or independent shop is covered before signing.

- Ask about exclusions: Pre-existing conditions are excluded from health plans. Pre-existing mechanical issues are excluded from warranty plans. Get clarity on what counts as a pre-existing condition before you commit.

The parallel is not just conceptual. Both types of plans reward members who read the fine print, verify their network, and activate every benefit they are entitled to.

Key takeaways

Essential plan coverage delivers far more value than most members realize, especially when you factor in dental, vision, wellness perks, and zero-deductible cost structures that eliminate financial barriers to care.

| Point | Details |

|---|---|

| Ten core benefits are mandatory | Every essential plan must cover hospital care, prescriptions, mental health, preventive services, and six other categories by law. |

| Dental and vision are included | Adult dental exams, cleanings, and annual vision exams with glasses or contacts are standard, not add-ons. |

| Wellness perks require activation | OTC allowances and gym reimbursements expire quarterly and must be claimed through a member rewards card. |

| Income bracket determines extras | Core medical coverage stays consistent across plan variants, but supplemental benefits and copays vary by income level. |

| Continuous enrollment is available | You can enroll year-round without waiting for open enrollment, which matters most when you lose employer coverage mid-year. |

What i've learned from watching people choose the wrong plan

I have spent years watching people select protection plans, whether health coverage or vehicle warranties, and the pattern of mistakes is almost identical every time. People focus on the monthly cost and ignore everything else. They see $0 premium and stop reading. They never check the network. They never activate the extras. Then they are surprised when a claim gets denied or a benefit expires unused.

The most overlooked feature in any essential plan is the wellness perks section. Gym reimbursements and OTC allowances sound minor until you calculate what they are worth annually. A quarterly OTC card worth $75 adds up to $300 per year. A gym reimbursement of $25 per month is another $300. That is $600 in real value sitting unclaimed in most member accounts.

The same blind spot shows up with vehicle warranty plans. Car owners buying coverage for a Honda Pilot or a Ford Explorer often skip past the roadside assistance and rental car reimbursement sections. Those benefits cost the provider money to include. If you are not using them, you are leaving value on the table.

My honest advice is to treat plan selection like a negotiation where you are the only one at the table. Read every benefit. Activate every perk. Verify every provider in your network before you need them. The plan that looks most expensive on paper often delivers the best value once you account for everything it covers.

Continuous enrollment is another underused advantage. Most people wait for open enrollment out of habit, not necessity. If your situation changes mid-year, apply immediately. Waiting costs you months of coverage you were already entitled to.

— Kenneth

Protect your vehicle with the right coverage from Rpmwarranty

Understanding how essential plan coverage works gives you a sharper eye for evaluating any protection plan, including the one covering your vehicle. Rpmwarranty offers extended vehicle warranty plans trusted by dealers nationwide, covering engines, transmissions, cooling systems, electrical components, and high-tech parts across a wide range of makes and models including BMW, Mercedes-Benz, Range Rover, Honda, Ford, and Porsche.

Every Rpmwarranty plan includes roadside assistance and is backed by a straightforward four-step process: consultation, plan selection, customization, and final agreement. You can compare protection plans by vehicle year, make, and model to find coverage that fits your budget and your car. Get a free quote today and make sure your vehicle is protected before the next repair bill arrives.

FAQ

What are the ten essential health benefits in an essential plan?

The ten core benefits are outpatient care, inpatient hospital care, emergency services, maternity and newborn care, mental health and substance use services, prescription drugs, rehabilitative and habilitative services, lab tests, preventive services, and pediatric services. Every essential plan must cover all ten by federal law.

Does an essential plan cover dental and vision for adults?

Yes. Essential plans include one annual dental exam, one cleaning, dental X-rays, and one annual vision exam with either prescription glasses or contact lenses. These benefits are standard coverage, not optional add-ons.

Who qualifies for an essential plan?

Adults ages 19–64 who earn up to 250% of the federal poverty level and meet legal residency requirements qualify. For a single-person household in New York, that income threshold is $39,125 per year.

Are there any premiums or deductibles in essential plans?

Most essential plan members pay $0 in monthly premiums and face no deductible. Copays apply to most services, but preventive care is always 100% free regardless of which plan variant you are enrolled in.

Can you enroll in an essential plan outside of open enrollment?

Yes. Essential plans allow continuous enrollment throughout the year. If you lose employer-sponsored coverage at any point, you can apply immediately without waiting for an open enrollment window.