TL;DR:

- Most vehicle owners overlook cancellation clauses, risking significant refunds when needed.

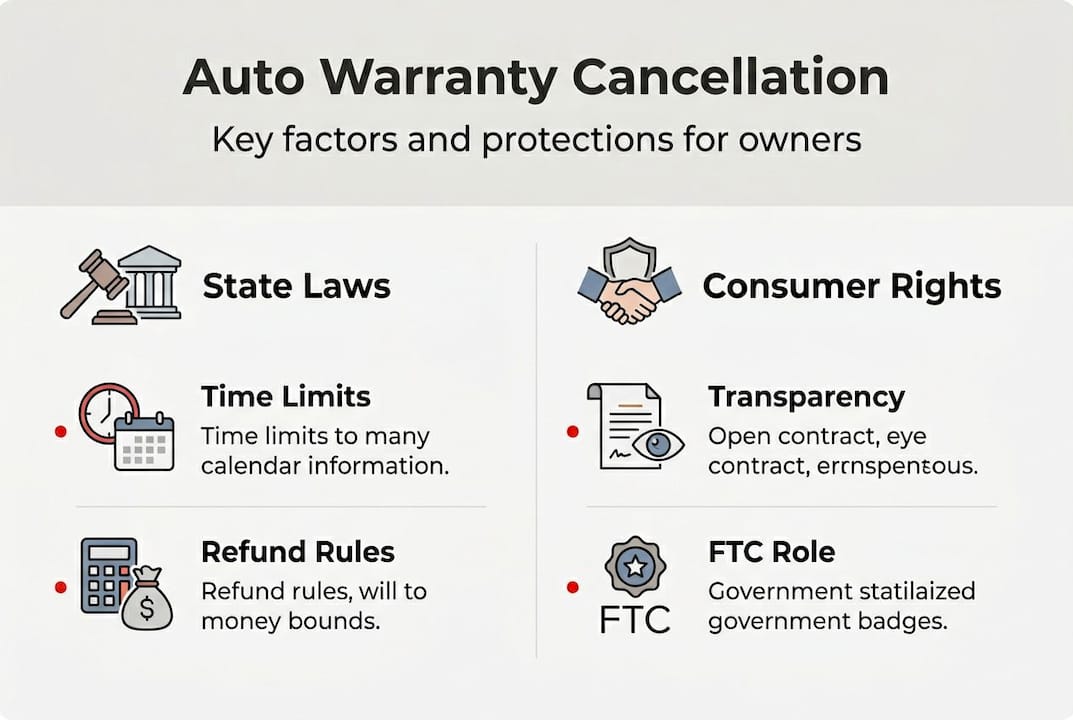

- Cancellation policies vary by state and provider, making it essential to read the contract carefully.

- Dealers often resist cancellations due to lost commissions, but direct provider contact and proper documentation can ensure success.

Most vehicle owners sign an extended warranty or vehicle service contract and never read the cancellation clause. That's a costly mistake. You might assume the contract locks you in permanently, but the reality is that cancellation is almost always an option. The catch? The rules vary by provider, state, and contract type. Dealers have a financial reason to keep you from canceling, and without knowing your rights, you could lose hundreds of dollars in refunds. This guide walks you through exactly how cancellation policies work, what state laws say, how to handle pushback, and how to make smart decisions before you ever sign.

Table of Contents

- What is a cancellation policy in auto warranties?

- Legal landscape: State laws, consumer rights, and FTC roles

- Why providers (and dealers) resist cancellations and how to respond

- Smart moves: How to maximize your cancellation rights and avoid common mistakes

- What most car owners get wrong (and how to avoid it)

- Explore your auto warranty options with confidence

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cancellation policies vary | Each warranty provider and state has unique rules, refund periods, and fees to know before canceling. |

| Know your rights | Reading your contract and understanding state protections can save money and reduce frustration. |

| Dealers may resist | Be prepared to escalate if your dealer or provider pushes back on a valid cancellation. |

| Act quickly | You’re more likely to get a full refund if you cancel early—often within a free-look period. |

| Choose reputable providers | The best protection starts with a trustworthy provider and transparent, detailed contract. |

What is a cancellation policy in auto warranties?

A cancellation policy is the set of rules inside your contract that spell out whether and how you can end the agreement before it expires. Think of it as the exit clause. It defines when you can cancel, what refund you're owed, how much you'll be charged in fees, and what documents you need to submit. Every contract handles this differently, which is why reading it before you sign matters enormously.

Before anything else, it helps to understand a critical distinction: most products sold as "extended warranties" are actually vehicle service contracts (VSCs). A true manufacturer warranty is a legal guarantee backed by the automaker. A VSC is a separate service agreement you buy from a dealer or third-party provider. This matters because no federal law mandates cancellation rights specifically for VSCs. Your contract itself is the governing document, which is why the cancellation clause deserves careful attention.

Here's what to look for in any cancellation policy:

- Refund eligibility: Is a refund guaranteed, prorated, or conditional?

- Timing windows: Does a "free-look" period apply (usually 30 days)?

- Administrative fees: Many contracts charge $25 to $75 to process a cancellation.

- Required documentation: Odometer reading, written notice, and sometimes notarization.

- Claims offset: If you've already used the contract for repairs, those costs may reduce your refund.

Some contracts buried in fine print will say cancellation is only allowed within the first 30 or 60 days. Others are more flexible. Understanding common car warranty myths can help you sort fact from fiction before assuming you're stuck. If you're just getting started, a beginner's guide to warranties covers the core concepts well.

You should also pay attention to what the contract actually covers. Knowing which covered and excluded items apply to your plan helps you evaluate whether it's worth keeping in the first place. And don't overlook warranty deductibles, which can quietly increase your out-of-pocket costs.

Pro Tip: Always request a copy of the full contract before finalizing any VSC purchase. If a dealer won't provide one, walk away.

With the basics established, it's important to understand how cancellation policies are shaped by where you live.

Legal landscape: State laws, consumer rights, and FTC roles

Knowing the standard elements of a cancellation policy, let's look at how the rules can differ widely depending on where you live and who regulates your contract.

There is no single federal law that gives you a guaranteed right to cancel a VSC. The Federal Trade Commission (FTC) plays a role, but it primarily targets deceptive or fraudulent practices, not the specific terms of individual cancellations. That means your biggest protections often come from state law, and those vary significantly.

State laws govern the specifics of VSC cancellations: California requires VSC sellers to maintain backup insurance, Florida mandates a full refund within 60 days of purchase, and at least 14 states require a 30-day free-look period during which you can cancel with no penalty.

Here's a quick comparison of how key states handle VSC cancellations:

| State | Free-look period | Full refund window | Notable rule |

|---|---|---|---|

| California | Varies by contract | Varies | Backup insurance required for VSC sellers |

| Florida | 30 days (common) | 60 days | Full refund if canceled within 60 days |

| Texas | 30 days | 30 days | Written notice required |

| New York | 30 days (some contracts) | Contract-specific | State regulates VSC as insurance |

| Other states (14+) | 30 days | Contract-specific | Mandatory free-look period |

"Understanding your state's specific rules is just as important as reading the contract itself. In some states, you have stronger protections than the contract language suggests."

If you live outside the states listed above, you're not necessarily unprotected. Many states have consumer protection statutes that cover unfair contract terms. The key is to check your specific state's laws before assuming you have no recourse.

Transparency matters here. A provider committed to warranty transparency will make cancellation terms easy to find and understand, not buried in paragraph 14 of a 40-page document.

Why providers (and dealers) resist cancellations and how to respond

After understanding your rights on paper, it's crucial to recognize the real-world obstacles you might face and how to beat them.

Dealers earn significant money on VSC sales. Dealer margins on VSCs average 50 to 70%, with average consumer payouts covering only 40 to 60% of the contract cost. That means a $2,000 warranty might net the dealer $1,000 to $1,400. When you cancel, that revenue disappears. Cancellation rates average 14.7% within the first 30 days, which tells you how common this conflict really is.

Here's what resistance often looks like:

| Tactic | What's really happening |

|---|---|

| "You can't cancel after signing" | False in most states; a bluff to discourage you |

| "The refund will take months" | Intentional delay to frustrate cancellation |

| "Only the dealer can process it" | Often untrue; providers usually handle directly |

| "There's a large fee" | Check your contract; fees are usually capped |

If you face pushback, dealerships may resist because of lost commission. Your best moves are to contact the warranty provider directly, document everything in writing, and escalate to your state attorney general or the FTC if the dealer stalls.

Here's a step-by-step action plan:

- Locate your contract and find the cancellation clause before making any calls.

- Contact the VSC provider directly, not the selling dealer, and request their official cancellation process.

- Submit written notice via certified mail with return receipt. Keep copies.

- Document every interaction: dates, names, call recordings if legal in your state.

- Track your refund timeline and follow up if payment doesn't arrive within the promised window.

- Escalate if needed: File complaints with the FTC, your state AG, or the Consumer Financial Protection Bureau.

Pro Tip: Knowing the key warranty features that reputable providers include can help you spot which providers are likely to honor cancellations smoothly. You can also review provider FAQs to understand what a transparent company looks like.

Smart moves: How to maximize your cancellation rights and avoid common mistakes

Let's put the knowledge together with expert-backed advice for making the smartest, safest moves with your warranty cancellation.

Timing is everything. Acting during the free-look period, if your state or contract offers one, is the single fastest path to a full refund with no fees. Once that window closes, your refund becomes prorated and fees apply.

Here are the smartest moves you can make:

- Read before you sign: Never skip the cancellation clause. If you don't understand it, ask for clarification in writing.

- Act fast: Cancel within the free-look period whenever possible.

- Keep every document: Purchase agreement, contract, correspondence, and refund confirmation.

- Avoid unsolicited offers: The FTC has sent over $96 million to consumers harmed by deceptively advertised VSCs, often pitched through unsolicited calls and mailers.

- Prefer reputable, manufacturer-backed plans when available.

- Choose third-party warranty providers who publish clear terms upfront.

Statistic to know: Consumer Reports has noted that most vehicle owners who purchase VSCs never use them, and the total cost often exceeds the value of repairs covered. This doesn't mean VSCs are never worth it, but it does mean you should evaluate your specific situation carefully.

Choosing a provider who makes customizing your warranty straightforward also reduces the chance of coverage mismatches that leave you paying out of pocket anyway.

Pro Tip: If you're financing a vehicle and the VSC is rolled into your loan, canceling the VSC should also trigger a refund applied to your loan balance. Confirm this with your lender in writing.

What most car owners get wrong (and how to avoid it)

Here's the uncomfortable truth most warranty articles won't say plainly: a lot of drivers buy VSCs because a dealer recommended it in a high-pressure finance office, not because they did independent research. That's a setup for overpaying.

The FTC has flagged billions in consumer harm tied to deceptive VSC practices, including misleading coverage claims and refusal to honor cancellations. This isn't an edge case. It's a pattern.

We've seen many vehicle owners focus entirely on what's covered and completely ignore the cancellation clause. That's like signing a lease without checking the early termination fee. The cancellation policy tells you how much you actually trust the company and the contract.

Manufacturer-backed or clearly detailed third-party contracts are almost always safer bets than vague, dealer-pushed VSCs. And sometimes, especially for newer vehicles with strong factory coverage or reliable makes, not buying an extended plan is genuinely the smarter financial move. The real skill is knowing which situation you're in before you commit.

Explore your auto warranty options with confidence

If reading through cancellation policies, state laws, and dealer resistance tactics has you feeling cautious, that's actually a good sign. It means you're thinking critically before committing.

RPM Warranty is built for vehicle owners who want real transparency, not boilerplate. Our Elite, Advanced, and Essential plans come with clearly stated terms, including cancellation policies you can actually read and understand. You can get a free quote tailored to your vehicle's year, make, and model, and compare coverage side by side without pressure. If you have specific questions before choosing, our FAQ page covers the details most providers gloss over. Protecting your vehicle shouldn't feel like a trap.

Frequently asked questions

Can you cancel an extended auto warranty at any time?

Cancellation eligibility and refund terms depend on your specific contract and your state's laws, so timing matters. Acting earlier in the contract term almost always means a larger refund and lower fees.

What is the typical refund if I cancel my car warranty early?

Refunds are usually prorated, meaning you get back the unused portion of what you paid, minus administrative fees and the value of any claims already paid out.

How do state laws affect my ability to cancel an auto warranty?

State law examples include California requiring backup insurance for VSC sellers, Florida offering a 60-day full refund window, and 14 states mandating 30-day free-look periods, but protections vary widely by location.

What should I do if a dealer resists my cancellation request?

Dealerships may resist because cancellations cost them commission, so your best move is to bypass the dealer, contact the VSC provider directly, document everything, and escalate to your state AG or the FTC if needed.

Are all auto warranty cancellation policies the same?

Contracts must specify the cancellation method, but provider policies and state laws vary significantly, which is why reading the fine print before signing is non-negotiable.