TL;DR:

- Carefully review coverage, exclusions, deductibles, and transfer conditions in vehicle service contracts.

- Verify the provider's license, obligor, and backup insurer to avoid scams or unpaid claims.

- Buy exclusionary plans from reputable sources, especially before factory warranties expire, for better protection.

Skipping the fine print on a vehicle service contract can cost you hundreds, sometimes thousands, of dollars when a repair claim gets denied. Many vehicle owners sign these agreements without fully understanding what they're buying, and that gap leads to real financial pain. Owners often pay more for extended warranties than they ever receive back in claims. This guide walks you through every section of a vehicle service contract so you know exactly what you're agreeing to, how to spot exclusions that could leave you stranded, and how to avoid the traps that catch most buyers off guard.

Table of Contents

- What is a vehicle service contract and why it matters

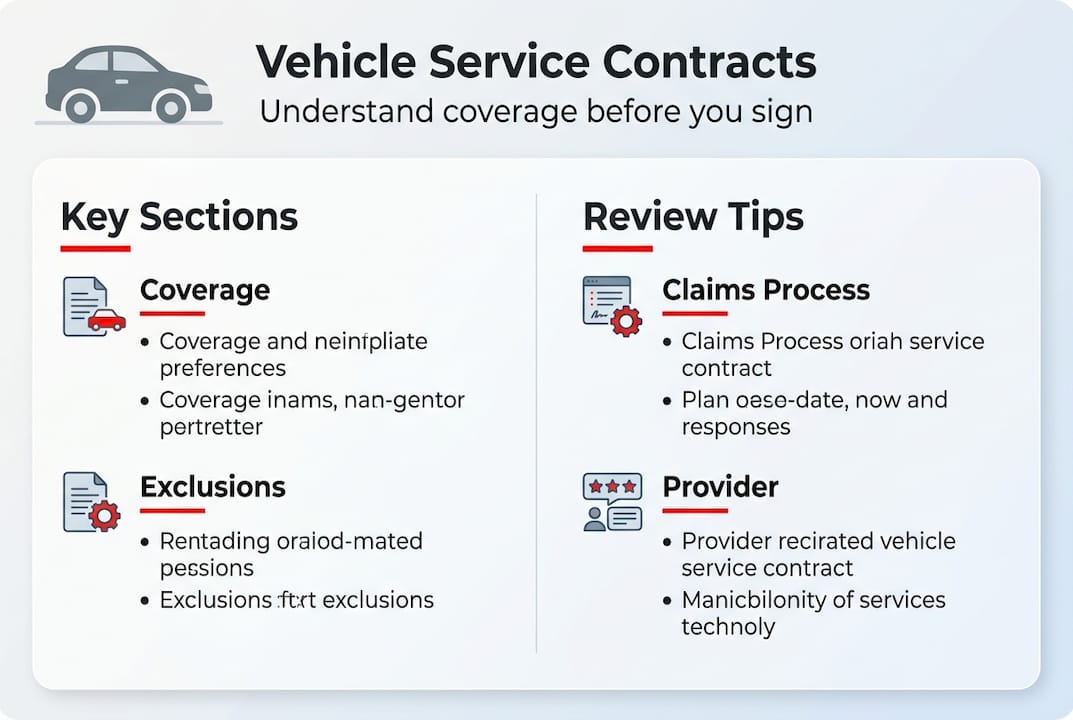

- Crucial sections to review in a vehicle service contract

- How to read coverage and exclusions: step-by-step

- Validating providers, licensing, and avoiding common traps

- Deciding if a vehicle service contract is worth it

- A fresh perspective: why contract details matter more than price

- Get reliable coverage from a trusted provider

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Check coverage and exclusions | Always read which parts and repairs the contract covers—and, more importantly, what it excludes. |

| Validate provider legitimacy | Confirm licensing, backup insurance, and the responsible obligor before signing. |

| Read claims rules carefully | Follow contract-specific claims steps or you may lose coverage for qualified repairs. |

| Understand if you need a VSC | These contracts may benefit high-mileage or unreliable vehicles, but are often unnecessary for reliable models. |

What is a vehicle service contract and why it matters

Before you read the fine print, it helps to know exactly what a vehicle service contract is and isn't.

A vehicle service contract, often called a VSC, is an optional agreement between you and a provider that covers the cost of certain repairs after your factory warranty expires. It is not insurance, and it is not the same as your manufacturer's warranty. Understanding that difference matters a lot when a claim gets denied.

Here's how the three main types of vehicle protection compare:

| Type | Who provides it | What it covers | Required? |

|---|---|---|---|

| Factory warranty | Manufacturer | Defects from production | Yes, included with new car |

| Vehicle service contract | Third party or dealer | Mechanical breakdowns post-factory | No, optional purchase |

| Auto insurance | Insurance company | Accidents, theft, liability | Yes, legally required |

As the California Department of Insurance explains, VSCs differ from insurance because they carry no accident coverage, and they differ from factory warranties because they are optional and purchased separately. Regulation also varies by state, so the protections you receive in one state may not apply in another.

Why does this matter for you? Because a misunderstood contract is the number one reason claims get denied. Buyers often assume a VSC works like insurance or like a manufacturer guarantee. It doesn't. Knowing the auto warranty basics before you sign protects you from that assumption.

Key reasons understanding your VSC matters:

- Denied claims often result from exclusions you didn't read

- Maintenance requirements buried in contracts can void coverage

- State-specific rules affect what backup protections you have

- Not all providers carry the financial backing to pay claims

"A vehicle service contract is not insurance. It is a separate agreement regulated differently by each state, and your protections depend heavily on who backs the contract." — California Department of Insurance

Reviewing the warranty service contract peace of mind factors before purchase gives you a clearer picture of what you're actually buying.

Crucial sections to review in a vehicle service contract

With the basics in mind, let's explore which contract sections matter most.

Every VSC is a legal document, and every section carries weight. Most buyers skim to the price and sign. That's a mistake. The California Department of Insurance identifies the key sections you must review: coverage details, exclusions, deductibles, claims process, duration, transferability, cancellation terms, and obligor information.

Here's a comparison of the two main contract types:

| Contract type | What it covers | Risk level for buyer |

|---|---|---|

| Inclusionary | Only named components | Higher — gaps are common |

| Exclusionary | Everything except listed exclusions | Lower — broader protection |

Always prefer an exclusionary contract. It covers more by default and limits the provider's ability to deny claims on technicalities.

Here are the sections to review in order:

- Coverage section: Lists exactly which components are protected. Look for engines, transmissions, cooling systems, and electrical systems.

- Exclusions section: This is where most claims die. Read every word. Look for wear-and-tear clauses and pre-existing condition language.

- Deductible terms: Some contracts charge per visit, others per repair. Per-repair deductibles cost more over time.

- Claims process: Does the contract require pre-authorization before repairs begin? Which repair shops are approved?

- Contract duration: Is coverage based on time, mileage, or both? Whichever limit hits first usually ends coverage.

- Transferability: Can you transfer coverage if you sell the car? This adds resale value.

- Cancellation terms: What's the refund policy if you cancel early?

- Obligor information: Who is legally responsible for paying your claim?

Pro Tip: Read the claims process section twice. Many buyers only discover pre-authorization requirements after a repair is already done, and that alone can void reimbursement.

You can review sample protection plans to see how transparent contracts lay out these sections clearly. Understanding protection features before comparing plans helps you ask the right questions. For a full breakdown of what clear contracts look like, the warranty coverage transparency guide is worth reading.

How to read coverage and exclusions: step-by-step

Now that you know the contract structure, here's how to read and interpret coverage and exclusions in detail.

Coverage and exclusions are the heart of any VSC. Getting this right is what separates buyers who get paid claims from those who get surprised bills.

Follow these steps to read coverage and exclusions accurately:

- List what you need covered. Before reading the contract, write down your car's most repair-prone systems. Then check if they appear in the coverage section.

- Cross-reference with exclusions. A component listed as covered may still be excluded under certain conditions. Read both sections together.

- Look for wear-and-tear language. This phrase is used to deny claims on parts that degrade over time, which includes a lot of mechanical components.

- Check maintenance requirements. Some contracts require proof of regular oil changes and inspections. Missing one service record can void your coverage.

- Identify the contract type. Is it inclusionary or exclusionary? The California Department of Insurance recommends exclusionary contracts for broader protection since they cover everything except what's specifically listed.

Watch for these red flags that signal a weak or predatory contract:

- Vague coverage language like "major components" without a specific list

- Long exclusions sections that are longer than the coverage section

- No mention of a backup insurer or obligor

- Requirements to use only one specific repair shop

- No cancellation or refund policy

Knowing what voids a car warranty is just as important as knowing what's covered. Many buyers lose coverage due to actions they didn't realize were prohibited.

Pro Tip: Always choose a broad, exclusionary contract from a reputable provider. A cheap inclusionary plan may look affordable upfront but leave you paying out of pocket for the exact repair you thought was covered. For a deeper look at what engine coverage actually includes, the engine coverage guide breaks it down clearly.

Validating providers, licensing, and avoiding common traps

After understanding coverage, the next critical step is confirming who stands behind your contract and that they're legitimate.

Not every company selling vehicle service contracts is financially sound or legally authorized. Some are outright scams. Others are legitimate businesses that lack the backing to pay large claims when they come in.

The California Department of Insurance advises buyers to verify the obligor, confirm a backup insurer exists for the vehicle service contract provider, and check that the seller is licensed. Avoid purchasing through unsolicited phone calls, internet pop-ups, or direct mail from unknown companies.

Here's a quick legitimacy checklist:

- The contract names a specific obligor (the party legally responsible for repairs)

- A backup insurer is listed in case the provider goes out of business

- The provider is licensed in your state

- A physical address and customer service number are easy to find

- The contract includes a free-look period (usually 30 days) to cancel without penalty

- No high-pressure sales tactics or demands for full upfront payment

State rules also matter. California, for example, requires backup insurance for VSC providers, which protects you if the company folds. High-mileage vehicles may also face additional restrictions depending on your state.

"Always verify the obligor and backup insurer before signing. If a seller cannot provide this information in writing, walk away." — California Department of Insurance

If you have questions about what legitimate coverage looks like, the warranty FAQ page covers the most common concerns buyers have before purchasing.

Deciding if a vehicle service contract is worth it

Once you understand how to spot a strong contract, it's time to ask if a VSC actually fits your needs.

The honest answer is: it depends. A VSC is not a smart buy for every vehicle or every owner. Consumer Reports notes that for reliable models, VSCs are often overpriced and unnecessary, but for unreliable or high-mileage vehicles with long ownership timelines, they can offer real value.

Who benefits most from a VSC:

- Owners of vehicles with known reliability issues or high repair costs

- Buyers keeping a car past 100,000 miles

- People who cannot absorb a sudden $2,000 to $4,000 repair bill

- Those buying used vehicles without remaining factory coverage

Who may safely skip it:

- Owners of highly reliable models with strong long-term track records

- People who plan to sell or trade the vehicle within two to three years

- Buyers with emergency savings that can cover unexpected repairs

- Those whose vehicles still have significant factory warranty remaining

The math is worth running. If your car's average annual repair cost is $400 and a VSC costs $1,800 over three years, you're likely paying more than you'll receive. But if one transmission replacement costs $3,500 and your VSC covers it, the contract paid for itself. Review the essential protection features to understand what components carry the highest repair costs before making your decision.

A fresh perspective: why contract details matter more than price

Stepping back, here's what most buyers overlook even after doing all the checklist steps above.

The biggest mistake we see is buyers choosing a VSC based on monthly cost rather than contract quality. A $60-per-month inclusionary plan sounds better than a $90-per-month exclusionary plan until the $3,000 repair you assumed was covered gets denied because of a single line in the exclusions section.

The Consumer Reports recommendation is clear: if you do buy a VSC, prioritize exclusionary contracts from reputable providers, ideally manufacturer-backed plans, and purchase while your factory warranty is still active. You get better terms, lower rates, and stronger protections when you buy early.

We've seen buyers get burned by flashy offers from companies with no physical address, no backup insurer, and no real claims process. The contract looked fine on the surface. The details told a different story. A $30 monthly savings is not worth a denied $4,000 claim. Read the contract first. Price is the last thing to evaluate, not the first.

Get reliable coverage from a trusted provider

If you're ready to put your knowledge into action, here's how to get coverage you can trust.

At RPMWarranty.com, we believe you should never have to guess what your contract covers. Our plans are built around transparency, with clear exclusionary coverage that tells you exactly what's protected and what isn't.

Whether you're comparing options or ready to commit, our vehicle protection plans cover engines, transmissions, electrical systems, and more, with nationwide service and straightforward claims. No surprises, no fine print traps. If you want to see what coverage looks like for your specific vehicle, you can get a free quote in minutes and compare plans side by side.

Frequently asked questions

What is the difference between a vehicle service contract and an extended warranty?

A vehicle service contract is an optional, post-factory repair agreement purchased separately from the manufacturer, while an extended warranty typically refers to manufacturer-provided protection that extends original coverage. As the California Department of Insurance clarifies, VSCs differ from both factory warranties and insurance in how they are regulated and what they cover.

What should I look for in a vehicle service contract?

Focus on coverage details, the full exclusions list, deductible structure, the claims process, duration limits, transferability, and obligor information. The California Department of Insurance identifies these as the key sections that determine whether a contract will actually protect you when repairs arise.

Are vehicle service contracts worth buying?

They can be worth it for high-mileage vehicles, unreliable models, or owners who can't absorb large repair costs, but most owners pay more in premiums than they receive back in claims for reliable vehicles.

How do I know if a contract provider is legitimate?

Verify the obligor, confirm a backup insurer is listed, and check that the provider is licensed in your state. The California Department of Insurance warns buyers to avoid unlicensed sellers and any company that contacts you through unsolicited calls or mail.