TL;DR:

- Most vehicle owners overlook their protection plans until facing costly repairs after the warranty expires, which is a costly mistake.

- Choosing the right coverage, understanding claim procedures, and reviewing contract details before purchase ensure better protection and avoid unexpected costs.

Most vehicle owners don't think about what happens after the factory warranty runs out until they're staring at a $4,000 transmission estimate with no warning and no plan. The vehicle protection plan workflow — from selecting the right coverage to managing claims without delays — is something most buyers skip over entirely. That is a costly mistake. This guide walks you through every stage: what these plans cover, how to prepare before you buy, how claims actually work, and how to avoid the contract traps that quietly kill your coverage when you need it most.

Table of Contents

- Understanding vehicle protection plans and their coverage

- Preparing to purchase a vehicle protection plan: What you need

- Executing the vehicle protection plan workflow: Managing claims and repairs

- Verifying benefits and avoiding common pitfalls in your vehicle protection plan

- A fresh take on vehicle protection plans: Beyond the sales pitch

- Exploring trusted vehicle protection plans to suit your needs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know coverage types | Understand the differences between powertrain, stated-component, and exclusionary protection plans for informed choices. |

| Review the entire contract | Carefully read coverage inclusions, exclusions, deductibles, and repair shop restrictions before purchasing. |

| Prepare key info | Gather vehicle age, mileage, and service history to compare plans and avoid surprises. |

| Understand claim steps | Know the diagnosis, pre-authorization, claims submission, and payment workflow to ensure smooth repairs. |

| Check repair flexibility | Plans allowing ASE-certified independent shops increase convenience and reduce downtime. |

Understanding vehicle protection plans and their coverage

An extended vehicle protection plan is a service contract that kicks in after your original manufacturer warranty expires. Unlike a manufacturer warranty, which is included in the price of the vehicle and covers factory defects, a protection plan is a separate agreement you purchase to cover mechanical failures beyond that window.

Extended warranties cover repairs after the manufacturer warranty expires, with coverage ranging from basic powertrain protection all the way to near-complete, exclusionary plans that list only what is not covered. The gap between those two ends of the spectrum is significant, and most buyers don't realize it until something breaks.

Here are the three main coverage types you will encounter:

- Powertrain coverage: Covers the engine, transmission, and drivetrain components. It is the most basic and affordable option, but it leaves out a lot. Electrical failures, cooling system issues, and high-tech components are typically not included.

- Stated-component coverage: A mid-tier option that names specific parts covered. You need to read this list carefully because "comprehensive-sounding" plans often leave out expensive components like the air conditioning compressor or power steering rack.

- Exclusionary coverage: Often called "bumper-to-bumper style," this plan covers everything except a specific list of exclusions. It is the most complete protection and works best for newer, lower-mileage vehicles.

Many plans also bundle in extras like roadside assistance, rental car reimbursement, towing benefits, and trip interruption coverage. These perks have real dollar value. A single roadside tow to a repair shop can run $150 or more depending on your location, so don't dismiss them as marketing fluff.

Preparing to purchase a vehicle protection plan: What you need

Walking into a plan purchase without preparation is how people end up locked into contracts that don't match their vehicles or their budgets. The auto protection plan process rewards those who do their homework first.

Your preparation checklist before purchasing should include:

- Current mileage and vehicle age: These two factors shape your eligibility and pricing more than almost anything else. Vehicle age and mileage affect which plans you qualify for and at what cost.

- Full service and repair history: Many contracts have maintenance requirements. If your records are incomplete, a provider can deny a claim by arguing the failure stemmed from neglect.

- Sample contract review: Before you pay anything, request a sample contract. Pull service history and read exclusions line by line. The exclusion list is where most plan disappointments hide.

- Deductible structure: Some plans charge a flat deductible per repair visit. Others charge per individual repair item, meaning a single visit with two separate repairs could cost you two deductibles.

- Repair shop rules: Find out whether the plan allows repairs at any ASE-certified (Automotive Service Excellence) independent shop or if it restricts you to dealerships only.

Pro Tip: Ask the provider specifically: "Can I use any ASE-certified shop, and will the adjuster pay them directly?" If the answer is vague or conditional, treat that as a red flag.

Here is a quick comparison of what to evaluate before signing:

| Factor | What to check | Why it matters |

|---|---|---|

| Deductible type | Per visit vs. per repair item | Affects out-of-pocket cost per claim |

| Shop flexibility | Any ASE shop vs. dealer-only | Impacts convenience and claim speed |

| Labor rate cap | Hourly rate the plan will reimburse | Can leave you paying the difference |

| Waiting period | Days/miles before coverage begins | Prevents immediate claims after purchase |

| Contract transfer | Can it go to a new owner if you sell? | Affects resale value of the vehicle |

Checking vehicle age, mileage, and prior repairs helps shape your eligibility and the true cost of any plan. Understanding deductible type and repair shop flexibility before you sign is what separates a smart purchase from an expensive regret. A thorough contract review is not optional — it is the single most important step in this entire process.

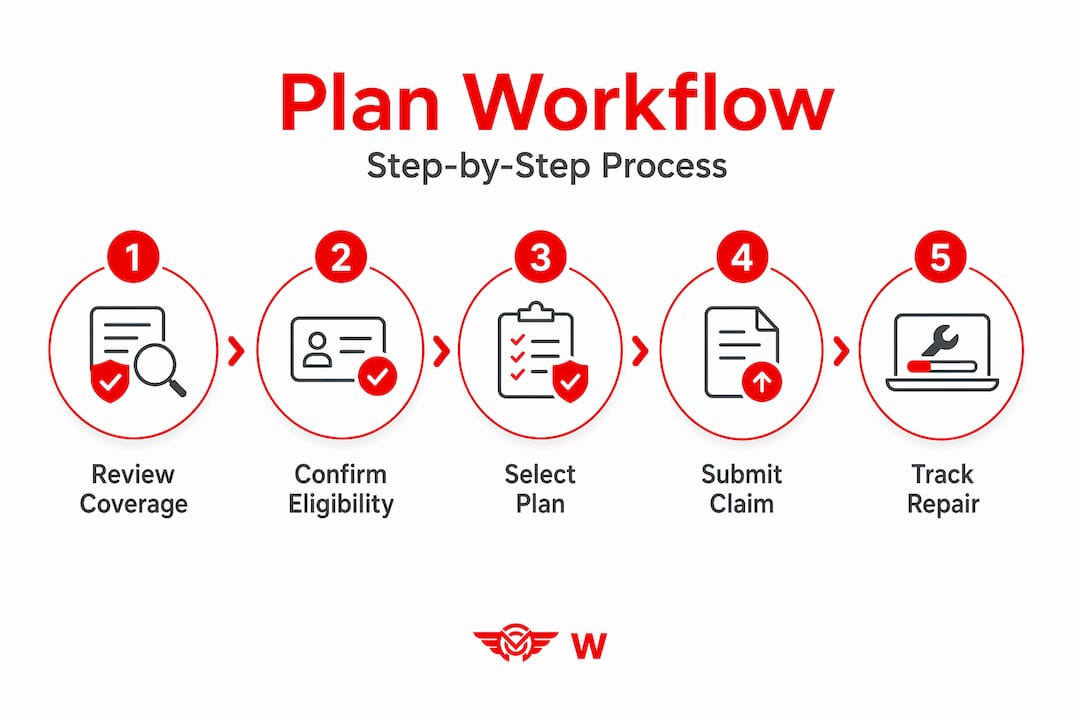

Executing the vehicle protection plan workflow: Managing claims and repairs

This is where the car coverage workflow either works for you or against you. Most owners don't think about the claims process until they are sitting in a repair shop waiting room. By then, any gaps in your preparation become expensive.

Here is how the claims process works from start to finish:

- Diagnosis and teardown authorization: Your repair shop diagnoses the problem. If the repair requires disassembly (called a teardown) to confirm the failure, most plans require pre-authorization before that step. Skipping this can void the claim entirely.

- Claim submission by the repair shop: The shop submits a detailed claim to the warranty provider. This includes the diagnostic fault codes, a parts list with costs, labor hours, and your vehicle's maintenance records. Verified diagnosis, pre-authorization, and detailed claim submission by the repair shop are required steps before any adjuster review begins.

- Adjuster review and approval: A claims adjuster reviews the submission, approves covered parts and labor hours, and issues a payment authorization directly to the shop. They may negotiate labor rates or substitute parts.

- Owner pays deductible and any gaps: You pay your deductible to the shop, plus any charges the plan did not cover, such as a labor rate above the plan's cap or non-covered items bundled into the same repair visit.

Pro Tip: Stay in contact with the shop during the adjuster review. If there is a dispute about a part or labor rate, your voice as the vehicle owner can sometimes accelerate resolution. Do not assume the shop will advocate on your behalf without prompting.

Here is how coverage scope and claim complexity differ by plan type:

| Plan type | Covered components | Claim complexity | Typical denial risk |

|---|---|---|---|

| Powertrain only | Engine, transmission, drivetrain | Low | Low, but narrow scope |

| Stated-component | Named parts list | Medium | Medium, gaps in coverage |

| Exclusionary | Everything except listed items | High | Low, but requires close reading |

For ongoing peace of mind with your service contract, keep a physical or digital folder with your contract, all service records, and every claim document. This habit pays for itself the first time a provider asks for proof.

Verifying benefits and avoiding common pitfalls in your vehicle protection plan

Buying the plan is only half the job. Getting full value from your automotive protection strategy means actively using and protecting your benefits.

Key habits to maintain throughout your coverage period:

- Keep dated maintenance receipts for oil changes, tire rotations, and any other service your contract requires. Poor maintenance records can cause claim rejection even when the failed part is clearly covered.

- Use your roadside assistance benefit before calling a towing company out of pocket. It is a paid benefit you are already entitled to.

- Claim rental car reimbursement when your vehicle is in the shop for a covered repair. Many owners forget this benefit exists.

- Watch for "dealer-only" repair restrictions in older or less reputable contracts. Contract terms on shop flexibility and preauthorization are often where hidden costs emerge.

- Review cancellation and transfer terms. If you sell the vehicle, a transferable plan increases its resale value. If you need to cancel, understand the prorated refund formula.

"The best plans cover roadside assistance, rental reimbursement, and allow repairs at ASE-certified shops. Vague contract language and dealer-only repair restrictions are the two most common sources of unexpected costs and denied claims."

Pro Tip: Before your first scheduled maintenance after purchasing a plan, re-read the maintenance requirements section of your contract. What counts as "adequate maintenance" is defined there, and some providers set higher bars than others.

Understanding exclusionary plan coverage details can help you evaluate whether a near-bumper-to-bumper plan justifies the higher premium versus a stated-component option for your vehicle's age and condition.

A fresh take on vehicle protection plans: Beyond the sales pitch

Here is what nobody in the extended warranty industry wants to say plainly: the monthly payment is the least important number in the entire transaction.

Providers compete on monthly price because it is the number most buyers focus on. But two plans at the same monthly cost can deliver completely different real-world protection. One might restrict you to dealership repairs, cap labor rates at $100 per hour in a market where shops charge $145, and charge a deductible per repair item rather than per visit. The other covers ASE-certified shops nationwide, reimburses at market labor rates, and charges one deductible per visit. The same premium. Wildly different coverage.

The speed of pre-authorization is also underrated. When your car is undrivable and sitting in a shop bay, every hour of adjuster delay is inconvenience and potentially a rental car expense. A provider with a 24-hour claims turnaround is meaningfully better than one that takes three business days, regardless of what their marketing says.

Self-insuring — setting aside money in a dedicated repair fund instead of buying a plan — is a legitimate strategy, but only if your fund can realistically absorb a $5,000 to $8,000 repair. That is the ballpark for a major engine or transmission replacement. Most owners overestimate how quickly they can build that cushion and underestimate how suddenly a major failure can arrive.

The smartest approach is to match your vehicle's specific repair risks with a contract's actual language. A 10-year-old vehicle with a known electrical complexity is a very different risk profile than a 6-year-old truck with a simple powertrain. Your plan should reflect that difference, not just a generic mileage bracket.

Exploring trusted vehicle protection plans to suit your needs

Understanding the workflow is one thing. Finding a provider who actually delivers on it is another.

RPM Warranty offers extended vehicle protection trusted by dealers nationwide, with a simple four-step process — consultation, plan selection, customization, and final agreement — that removes the guesswork from the auto protection plan process. Whether you need powertrain-only protection or near-bumper-to-bumper exclusionary coverage, the available protection plans are built to match your vehicle's age, mileage, and risk profile. Benefits include roadside assistance, rental coverage, and nationwide repair access. Pricing is transparent, and you can compare free quotes based on your vehicle's specific year, make, and model — without any obligation.

Frequently asked questions

What is a vehicle protection plan workflow?

It is the step-by-step process vehicle owners follow from selecting an extended warranty through managing claims and repairs to ensure proper coverage and cost control.

How do vehicle protection plans differ from original manufacturer warranties?

Original warranties cover defects for a limited time. Manufacturer warranty vs. service contract differences come down to duration, scope, and flexibility. Vehicle protection plans extend coverage afterward with customizable options.

Can I use any repair shop for claims under an extended vehicle protection plan?

Some plans allow repairs at any ASE-certified independent repair shop, while others restrict service to dealerships. Plans allowing ASE-certified shops usually create smoother, faster claims than dealer-only restrictions.

What should I look for in the fine print of a vehicle protection plan?

Focus on coverage inclusions and exclusions, deductible structure, waiting periods, labor reimbursement rates, and repair shop flexibility. Contract details like deductibles and labor limits determine real coverage value.

Are all extended vehicle protection plans worth the cost?

Value depends on your vehicle's age, mileage, repair risk, and whether an unexpected repair would cause financial strain. Extended warranty value depends on owner preference for predictable monthly costs versus the risk of a major unplanned repair bill.