TL;DR:

- Engine coverage primarily pays for repairs to specific internal engine parts due to mechanical failure, not all engine issues. It excludes routine maintenance, pre-existing conditions, and damage caused by neglect, requiring owners to understand their policy's fine print. Proper documentation, maintenance, and selecting the right plan level based on vehicle age and usage can maximize protection and avoid claim denials.

Most car owners assume that signing up for engine coverage means any engine repair is automatically paid for. Then the bill arrives, the claim gets denied, and suddenly "engine coverage" feels like a broken promise. The reality is more nuanced, and understanding exactly what engine coverage includes, what it excludes, and how to use it properly can save you thousands of dollars over the life of your vehicle. This guide breaks it all down in plain language so you can make smart decisions before a problem hits.

Table of Contents

- What is engine coverage? Defining the basics

- What does engine coverage include, and what does it exclude?

- How engine coverage compares to other warranty options

- What to watch out for: Pitfalls, edge cases, and coverage tips

- Our take: The truth about engine coverage most owners miss

- Protect your investment with trusted engine coverage options

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Engine coverage basics | Engine coverage pays for repairs to select engine parts but not all causes of engine failure. |

| Common exclusions | Policies typically exclude pre-existing issues, lack of maintenance, and some types of damage. |

| Comparison is key | Engine, powertrain, and bumper-to-bumper warranties each protect different vehicle parts. |

| Avoiding denial | Proper upkeep and knowing contract details helps prevent denied coverage claims. |

| Right protection choice | Comparing options and reading fine print ensures you pick the right coverage for your needs. |

What is engine coverage? Defining the basics

Let's start by clearing up what engine coverage really means and what it protects.

Engine coverage is a type of vehicle protection that pays for repairs to specific internal engine components when they fail due to a mechanical breakdown. It is not a blanket promise to fix everything under the hood. Instead, it covers a defined list of parts, and your contract spells out exactly which ones qualify.

Typical components covered under engine coverage include the cylinder block and cylinder heads, pistons and piston rings, the crankshaft and connecting rods, the camshaft and camshaft bearings, the timing chain or timing belt, oil pump, valve springs, and intake and exhaust valves. These are the parts that keep combustion happening and the engine running. When one fails due to a mechanical defect rather than neglect, engine coverage steps in.

Understanding the engine warranty coverage basics before you buy a plan is just as important as shopping for the plan itself. Many owners skip this step and pay for it later.

| What is typically covered | What is typically NOT covered |

|---|---|

| Cylinder block and heads | Routine oil changes and filters |

| Pistons, rings, and rod bearings | Normal wear and tear |

| Crankshaft and main bearings | Damage from neglect or lack of maintenance |

| Timing chain, gears, and guides | Pre-existing conditions |

| Oil pump and water pump (in some plans) | External hoses and belts |

| Camshaft and cam bearings | Damage from overheating due to owner neglect |

| Valve train components | Catalytic converter |

Here is a quick snapshot to keep in mind:

Typically covered:

- Internal lubricated engine parts

- Seals and gaskets directly related to covered components (policy-dependent)

- Timing components and valvetrain parts

- Mechanical failures caused by a defect

Common surprises (not covered):

- Any repair tied to missed oil changes

- Damage that began before your policy started

- Repairs filed during a waiting period

- Failures caused by an excluded component that then damaged a covered one

Automotive warranty transparency is something every reputable provider should offer upfront. If a company makes it hard to find what is and is not covered, that is a red flag worth taking seriously. Always read the sample contract before committing, and consider consulting auto repair specialists who can help you understand what breakdowns are most likely given your vehicle's age and mileage.

Common edge cases that can affect whether engine repairs are covered include maintenance record requirements, pre-existing conditions, consequential damage vs. the initially failed component, and waiting periods. These details live in the fine print, and they matter more than most owners realize at purchase time.

What does engine coverage include, and what does it exclude?

Now that you understand the basics, let's dig into the fine print, what's actually included and where owners get tripped up.

Inclusions: What you can typically expect

Covered failures generally involve internal mechanical components that break down without a contributing cause on the owner's end. Think of a crankshaft bearing that fails at 80,000 miles with no history of missed oil changes. That is exactly the scenario engine coverage is designed for. Seals and gaskets are sometimes included but only when they fail as a direct result of a covered component's failure. This distinction matters a lot when you file a claim.

Exclusions: Where most claims fall apart

Here is where it gets uncomfortable for many owners:

- Maintenance-related failures: If your engine seizes because you went 15,000 miles between oil changes, that is a maintenance failure, not a mechanical defect.

- Pre-existing conditions: Any issue that existed before your coverage started is excluded, full stop.

- Waiting period denials: Most policies include a waiting period of 30 days or a set mileage threshold before you can file a claim.

- Consequential damage: If an excluded part fails and then destroys a covered part, the covered part's repair may still be denied.

- Overheating damage: If your coolant light came on and you kept driving, any resulting engine damage is typically on you.

"Exclusions can also deny consequential damage when an excluded cause is involved." This means even a covered part can be denied if the root cause of its failure was something your policy does not cover.

Real-world scenario: A driver purchases engine coverage and three months later notices a knock in the engine. The repair shop diagnoses a failed rod bearing. The warranty provider reviews the claim and finds no oil change records on file and evidence that the oil was dangerously low. Claim denied. The driver is on the hook for a $4,200 repair.

Understanding exclusionary warranty details ahead of time makes the difference between a smooth claim and a frustrating denial. Some providers also offer add-on protection features like rental car reimbursement and roadside assistance that can soften the impact of a repair even when the main claim has complications.

Pro Tip: Start a simple maintenance log the moment you buy engine coverage. Keep oil change receipts, filter replacements, and any service records in a single folder, either physical or digital. This documentation is your strongest defense if a claim is ever questioned.

How engine coverage compares to other warranty options

Understanding exclusions is key, but it is also smart to see how engine coverage compares to broader or narrower warranty options.

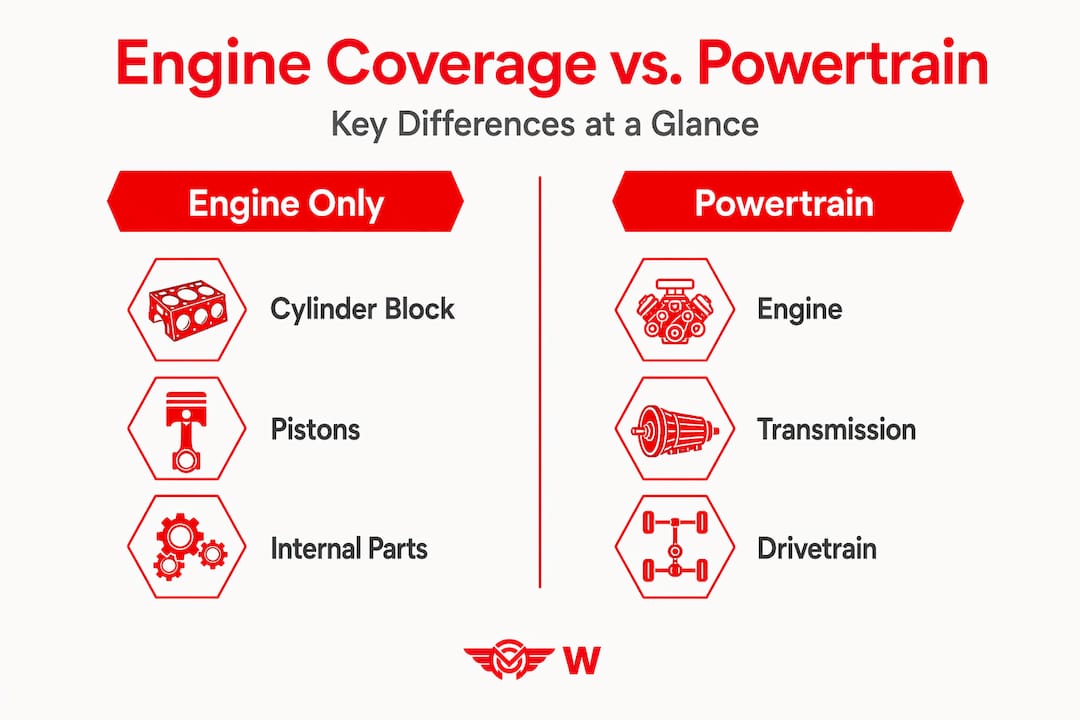

Engine coverage is focused. It protects the internal components of your engine and little else. That can be exactly right for some owners, but others need more.

| Warranty type | Engine | Transmission | Drivetrain | Electronics | A/C and cooling |

|---|---|---|---|---|---|

| Engine only | ✓ | ✗ | ✗ | ✗ | ✗ |

| Powertrain | ✓ | ✓ | ✓ | ✗ | ✗ |

| Bumper-to-bumper | ✓ | ✓ | ✓ | ✓ | ✓ |

A powertrain warranty comparison shows that powertrain plans extend protection to the transmission and drivetrain, which are expensive repairs in their own right. A transmission replacement can run $3,500 to $8,000 depending on the vehicle. Engine-only coverage would leave you fully exposed to that cost.

Bumper-to-bumper plans cover nearly everything, including electronics, air conditioning, suspension components, and more. For a newer vehicle or one loaded with technology, this level of protection is often worth the additional premium. The bumper-to-bumper vs powertrain comparison comes down to how much exposure you can afford and how complex your vehicle is.

Steps for choosing the right coverage level:

- Assess your vehicle's age and mileage. Older vehicles with high mileage tend to have more component failures across multiple systems, not just the engine.

- Review your budget for monthly premiums vs. out-of-pocket risk. Calculate what you could reasonably absorb in a single repair bill before deciding on a plan tier.

- Research your vehicle's known failure points. Some makes and models have documented weak spots in their transmissions or electrical systems. Check owner forums and repair data.

- Consider your driving habits. High-mileage drivers or those who tow frequently put more stress on drivetrain components, making broader coverage more valuable.

- Compare deductible structures. Some plans use a per-visit deductible, while others charge per component. This affects your real cost in a multi-part claim.

Drivetrain warranty details are especially relevant if you drive a four-wheel-drive or all-wheel-drive vehicle, where drivetrain components wear faster and repairs cost more.

Not all warranties are right for every car or every owner. A high-mileage commuter vehicle and a low-mileage weekend car carry very different risk profiles, and your coverage should reflect that.

What to watch out for: Pitfalls, edge cases, and coverage tips

With all options on the table, knowing where coverage can go wrong helps you avoid expensive surprises.

Many claim denials come down to a handful of predictable mistakes. The good news is that most of them are completely avoidable with a little preparation.

Top pitfalls that lead to denied claims:

- Missing maintenance records: You do not need to use a dealership for oil changes, but you do need proof that you got them done consistently.

- Filing too soon: Some contracts may deny if you file within a waiting period or if the provider concludes the failure started before coverage began. This is one of the most common and most frustrating denial reasons.

- Delayed reporting: If you notice a problem and keep driving, the damage that accumulates after that point may not be covered.

- Using non-approved repair shops: Some plans require you to use a network shop or get prior authorization before repairs begin. Skipping this step can void a claim entirely.

- Ignoring warning lights: Continuing to drive with a check engine light or oil pressure warning is often treated as owner negligence in a claim review.

Edge cases worth knowing:

- A provider may deny a claim for a component that technically falls under coverage if they can demonstrate the failure started before the policy effective date. This is called a pre-existing condition determination, and it can be frustratingly subjective.

- Consequential damage is tricky. If your oil pump fails (a covered part) and then destroys your bearings, that chain of events might be covered. But if an oil leak caused by a non-covered hose destroys a covered bearing, that is a different story entirely.

Tips to protect your coverage:

- Keep all maintenance receipts in a dedicated folder

- Follow the manufacturer's recommended service intervals, not just the minimum

- Report any warning lights or changes in engine behavior promptly

- Always get pre-authorization from your warranty provider before major repairs

- Review your specific contract for the waiting period terms before you expect to file

Pro Tip: Read the waiting period terms the day you purchase your plan, not when a problem arises. Knowing that your plan has a 30-day or 1,000-mile waiting period helps you avoid a costly claim denial if something goes wrong early in your coverage period.

Understanding warranty voiding risks is essential reading for any new coverage holder. And if the standard plan does not match your needs, customizing warranty coverage to fit your specific vehicle and driving situation is always an option.

Our take: The truth about engine coverage most owners miss

Having covered the facts and risks, here is a perspective few guides share, one shaped by years of experience in automotive protection.

Engine coverage is genuinely valuable. A single catastrophic engine failure can cost $5,000 to $10,000 or more, and without protection, that bill falls entirely on you. But here is the uncomfortable truth: the owners who benefit most from engine coverage are not the ones who rely on it. They are the ones who treat their vehicles well and use the coverage as a safety net rather than a substitute for good habits.

We see this pattern repeatedly. A driver with meticulous maintenance records files a claim after a legitimate mechanical failure, and the process is smooth. Another driver with no documentation files a claim for what might have been a covered repair, but without records, the provider has reasonable grounds to deny it. Same coverage, completely different outcomes.

The counterintuitive advice here is this: treat engine coverage as your backup plan, not your primary plan. Your primary plan should be consistent maintenance, timely oil changes, and listening to your vehicle when it tells you something is wrong. Engine coverage is what protects you when everything else goes right but something mechanical still fails.

There is an idea worth keeping close: "The best warranty is the one you never need." That sounds like a dismissal of coverage, but it is not. It is a reminder that coverage works best when it is paired with a vehicle owner who is paying attention. Real-world warranty examples consistently show that documented, proactive owners have far fewer claim denials than owners who treat coverage as a hands-off solution.

One more thing worth noting: too many owners only discover the limits of their coverage after a costly denial. Do not be that person. Read the contract, ask questions before you buy, and know your exclusions cold. That knowledge alone is worth more than any single claim.

Protect your investment with trusted engine coverage options

Ready to turn knowledge into true protection? Here is how you can choose coverage with confidence.

Now that you know how engine coverage works, what it covers, and where it can fall short, the next smart move is finding a plan that matches your vehicle and your budget. Reputable providers offer transparent terms, flexible options, and clear claims processes so you are never left guessing.

At RPM Warranty, you can explore engine coverage plans across three tiers, Elite, Advanced, and Essential, designed to fit different needs and price points. Whether you want focused engine protection or broader coverage that extends to your transmission, cooling system, and electrical components, there is an option built for you. The best way to find your fit is to get a free coverage quote based on your vehicle's year, make, and model. It takes minutes and gives you a concrete starting point for protecting your investment.

Frequently asked questions

Does engine coverage include wear-and-tear repairs?

Engine coverage usually does not include repairs caused by normal wear and tear or routine maintenance, as maintenance exclusions are standard across most policies.

Is engine coverage the same as powertrain warranty?

No, powertrain warranties cover more components than just the engine, including the transmission and drivetrain, making them a broader form of protection.

Can my engine claim be denied if I miss oil changes?

Yes, missing required maintenance like oil changes can lead to denied engine coverage claims, since proper maintenance documentation is often a contract requirement.

Will engine coverage pay for a pre-existing problem?

No, issues that started before your coverage began are typically excluded, since pre-existing conditions are one of the most common denial reasons in engine coverage claims.